The Long Island housing market has always moved to its own rhythm—shaped by proximity to New York City, limited inventory, and fierce demand from buyers who want suburban space without sacrificing access to urban careers. But in 2026, sellers face a landscape that’s shifting faster than ever. Although interest rates have stabilized after years of volatility, buyer behavior has changed. Inventory remains tight in some pockets while easing in others. And for homeowners in distress situations—divorce, foreclosure, probate—understanding these Long Island real estate trends isn’t just helpful. It’s urgent.

If you’re considering selling, whether by choice or circumstance, the decisions you make today will directly impact how much you walk away with and how quickly you can move on. Therefore, here’s what’s really happening in Nassau and Suffolk counties, and what it means for your sale.

Long Island Real Estate 2026

Market Intelligence for Nassau & Suffolk Sellers

Market Stable

Rates at mid-6%. Buyers selective, want move-in ready homes.

Buyer Shift

Turnkey or major discounts. Moderate repairs don’t sell.

Time = Money

90+ days on market = 3-7% lower price.

Nassau County

- $650K-$750K median

- 45-60 days on market

- Tight inventory

- Turnkey expected

Suffolk County

- $450K-$900K range

- Diverse markets

- Rising inventory

- Waterfront premium

6-Month Holding Costs

| Expense | Monthly | Total |

|---|---|---|

| Mortgage | $3,200 | $19,200 |

| Property Tax | $900 | $5,400 |

| Utilities/Insurance | $500 | $3,000 |

| Maintenance | $200 | $1,200 |

| Total | $4,800 | $28,800 |

Critical for Distressed Sellers

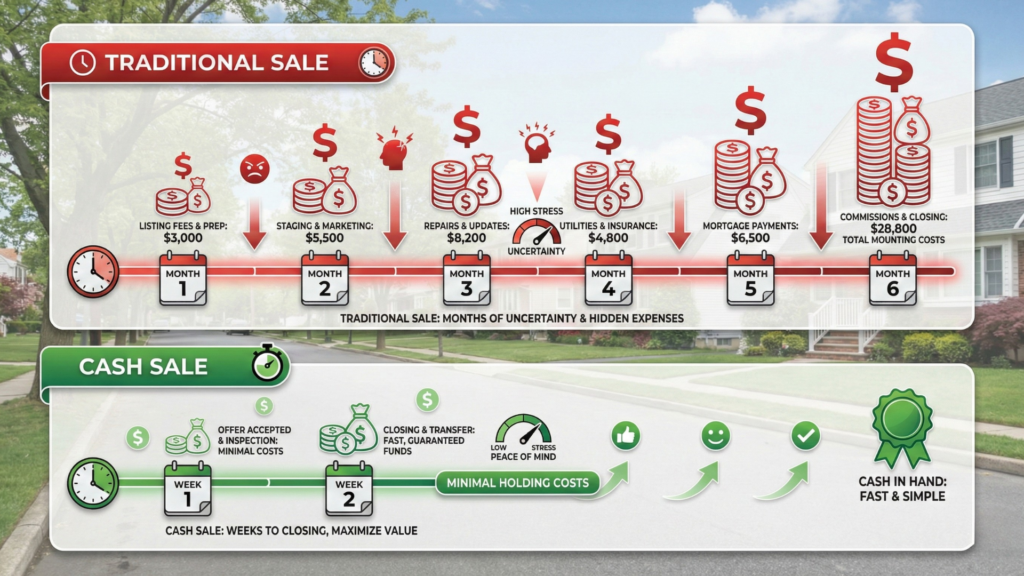

Waiting for “better conditions” costs more in holding expenses than appreciation gains. Cash sales = no repairs, showings, or delays.

Why Long Island Real Estate Trends Matter More Than National Headlines

National housing reports can’t tell you what’s happening on your street. In fact, Long Island operates as a cluster of micro-markets—some neighborhoods see bidding wars while others sit stagnant for months. The difference often comes down to school district quality, commute times, waterfront access, and local economic conditions.

In 2026, several factors are reshaping the Long Island real estate trends landscape. After climbing to 7%+ in 2023–2024, interest rates have finally settled into the mid-6% range. As a result, local MLS market data from early 2026 shows 30-year fixed rates in New York recently dipping near 6.11%, bringing fence-sitters back into the market without sparking the frenzy many predicted. Today’s buyers are also pickier—they want move-in ready homes or significant discounts for fixer-uppers. Consequently, the middle ground, homes that need moderate work, often languishes.

Nassau County’s Gold Coast and South Shore remain starved for listings, with inventory plummeting 16.8% year-over-year in January 2026 per OneKey MLS FastStats, while some outer Suffolk areas like Riverhead and Brookhaven have seen modest inventory increases. Meanwhile, demographic shifts are reshaping demand as well, with younger buyers prioritizing affordability over prestige zip codes and empty nesters downsizing or leaving Long Island entirely for lower-tax states.

For sellers, this means one-size-fits-all advice doesn’t work. For example, a waterfront home in Huntington operates in a completely different market than a ranch in Patchogue. Similarly, a seller facing foreclosure in Suffolk County has different urgency and options than someone casually testing the market in Nassau County.

Suffolk County vs Nassau County: Two Markets, Two Strategies

Nassau County: Tight Inventory, High Expectations

Nassau County continues to benefit from its reputation—better schools, shorter commutes, established neighborhoods. However, that prestige comes with higher property taxes and buyer expectations that match the price tags.

Current Nassau County market conditions reflect just how competitive things have become: single-family median home prices reached $835,000 in January 2026, up 3.1% year-over-year, per OneKey MLS FastStats data. Single-family homes average approximately 55 days on market—down 16.7% from a year earlier—as inventory of single-family homes fell 16.8% to 1,497 units in January. As a result, buyers expect turnkey condition or price adjustments that reflect renovation costs. The luxury market ($1M+), on the other hand, has softened somewhat, with longer selling times.

If you’re selling in Nassau County, presentation matters enormously. Homes that show well—fresh paint, updated kitchens, neutral finishes—move faster. In contrast, homes that need work often face price negotiations that exceed the cost of the repairs themselves. For sellers dealing with inherited property or probate sales, this creates a real dilemma: invest in repairs you may never recoup, or accept a lower offer from a cash buyer who will handle the work instead. Learn more about the specific challenges and opportunities for Nassau County home sellers.

Suffolk County: Diverse Markets, More Flexibility

Suffolk County, by contrast, offers more variety—from the affluent North Shore to the working-class communities of central Suffolk to the beaches of the South Shore. This diversity means sellers have more options, but also face more competition depending on location.

Current Suffolk County market conditions: single-family home prices hit a record median of $725,000 in November 2025 per OneKey MLS, up from $702,000 in July 2025—the first time the county median had ever crossed $700,000. Furthermore, Redfin’s January 2026 data shows the all-property-type median at $675,000, up 4.3% year-over-year, with homes averaging 37 days on market. Inventory remains tight at roughly 3 months of supply countywide. Lower-cost commuter towns in central Suffolk start around $550,000–$600,000 for older stock needing updates, while waterfront and beachfront properties in desirable areas still routinely exceed $900,000.

Suffolk County sellers have more flexibility with pricing strategy, but that also means more room for error. Overpricing in a market with rising outer-area inventory means your home sits, grows stale, and eventually sells for less than if you’d priced it right from the start. For homeowners in distress—facing foreclosure or selling during divorce—waiting for the “perfect” buyer can therefore mean losing more equity to holding costs, legal fees, or mortgage arrears.

For more guidance on county-specific selling strategies, see our detailed pages for Suffolk County home sellers and Nassau County. Specific towns like Babylon and Patchogue each have unique market characteristics that are also worth understanding.

How Long Island Real Estate Trends Impact Distressed Sellers

Market trends that seem abstract become painfully concrete when you’re selling under pressure. Let’s connect the dots between what’s happening in 2026 and what it means if you’re facing a forced sale.

Divorce: When Time Equals Money Lost

In a divorce sale, every month of delay costs you. Mortgage payments, property taxes, insurance, utilities—these holding costs steadily drain the equity you’re trying to divide. Meanwhile, Long Island real estate trends show that homes sitting on the market past 90 days start losing negotiating power. Buyers smell desperation.

Traditional listings in divorce situations often fail because both parties must agree on price, repairs, and showing schedules; homes in dispute often aren’t maintained, which buyers quickly notice; and emotional conflict delays decisions at every step. Cash sales, however, remove these friction points entirely. One offer, one closing date, one division of proceeds. No repairs, no showings, no waiting for buyer financing to fall through. As a result, our complete guide on selling your house during divorce on Long Island is worth reading before you decide how to proceed.

Pre-Foreclosure: The Clock Doesn’t Care About Market Conditions

If you’re behind on payments, Long Island real estate trends are essentially irrelevant compared to your foreclosure timeline. New York’s judicial foreclosure process averages approximately 445 days—about 15 months from the first missed payment to the foreclosure sale—according to the NY Department of Financial Services, making New York the state with the longest average foreclosure timeline in the country. Once the process starts, moreover, your credit is damaged and your options narrow with every passing month.

The current market does offer some advantages: home values have held relatively steady, so you likely still have some equity; lenders are still motivated to avoid foreclosure costs; and cash buyers can close fast enough to stop the process altogether. But you need to act before the foreclosure auction is scheduled. After that point, your ability to sell traditionally evaporates. Learn more about your options for pre-foreclosure sales and understand how fast you can actually sell a house for cash.

Inherited Property: Market Timing You Didn’t Choose

Inheriting a Long Island home should feel like a gift, but it often feels like a burden instead—especially when property taxes, maintenance, and family disagreements pile up. The current market doesn’t favor inherited homes that need work, yet many inherited properties come with exactly that problem.

Buyers expect discounts for dated kitchens, old systems, and deferred maintenance. Multiple heirs also complicate decision-making. Furthermore, probate delays mean property taxes and utilities drain value while you wait. Selling inherited property to a cash buyer, therefore, means skipping the repair debate entirely. The buyer takes the property as-is, often covering closing costs, and closes quickly enough to stop the financial bleed. Our guide on selling an inherited house in New York covers the specific legal and financial considerations you’ll need to understand.

For the complete guide on selling your Long Island home fast, see our comprehensive resource.

The Real Cost of “Waiting for the Right Market”

One of the most damaging Long Island real estate trends myths is that waiting for better conditions will net you more money. In reality, the math rarely works that way—especially for distressed sellers.

Holding Costs Compound Quickly

To illustrate, let’s run real numbers for a typical Long Island home:

| Expense | Monthly Cost | 6-Month Total |

|---|---|---|

| Mortgage (PITI) | $3,200 | $19,200 |

| Property Taxes (Suffolk avg) | $900 | $5,400 |

| Utilities | $350 | $2,100 |

| Insurance | $150 | $900 |

| Maintenance/Repairs | $200 | $1,200 |

| Total | $4,800 | $28,800 |

If you wait six months hoping for a better market, you’ve already spent nearly $29,000 in holding costs. Even if the market improves by 3–5% during that time, you’ve likely lost ground compared to selling quickly at a slightly lower price. Understanding when selling to an investor makes sense versus waiting often comes down to exactly this calculation.calculation.

Market Appreciation Is Not Guaranteed

Long Island real estate trends show that appreciation has slowed significantly from the 2020–2022 boom years. In 2026, annual appreciation in most Long Island markets is running 3–5% per OneKey MLS and Redfin data—meaningful, but not enough to offset holding costs on a vacant or near-vacant property. Additionally, Long Island inventory overall remains at roughly 3 months of supply, about half the 6-month level associated with a balanced market, per local MLS data from early 2026.

For sellers who need to move quickly—job relocation, health crisis, family changes—waiting for appreciation is therefore a gamble you’re likely to lose. The guaranteed costs exceed the potential gains in most scenarios.

Stigma of a Stale Listing

Homes that sit on the market send a clear signal: something’s wrong. Maybe it’s overpriced, maybe it needs work, or maybe the location isn’t desirable. Either way, buyers and their agents notice. After 90 days, you’re no longer a fresh listing competing for attention—you’re the house everyone has already passed on.

This stigma is real and measurable. Data from Long Island MLS systems consistently shows that homes selling in the first 30 days command 3–7% higher prices than comparable homes taking 90+ days, even after accounting for differences in condition and location.

When Selling As-Is Makes More Sense Than Renovating

The Long Island real estate trends in 2026 reveal a clear divide: move-in ready homes sell quickly, while homes needing significant work face steep discounts. This creates a false choice for many sellers—invest thousands in repairs you may not recoup, or list as-is and accept lowball offers. Fortunately, cash buyers offer a third option: sell as-is without renovating, but also without enduring months of price cuts and failed negotiations. Understanding what selling as-is really means helps clarify this option.

The Renovation Break-Even Myth

Real estate agents often suggest renovations to “maximize value,” but the Long Island real estate trends show that many renovations simply don’t pay for themselves in a sale. Kitchen remodels typically recoup 50–70% of costs; bathroom updates return 60–75% on average; and cosmetic fixes (paint, flooring) return better percentages but still cost thousands upfront. Homes in probate or divorce situations, furthermore, often can’t justify these expenses—or the time they require.

The question of whether you should repair your house before selling has a different answer depending on your timeline and financial situation. In either case, cash buyers make offers based on current condition, eliminating the renovation gamble entirely.

What “As-Is” Really Means

Selling as-is means no repair negotiations after inspection, no updating systems or finishes before listing, no staging or showing prep, and a single offer that accounts for all needed work upfront. With current Long Island real estate trends showing buyers demanding credits and concessions during traditional sales, the simplicity of an as-is cash sale therefore has real value. The price is the price—no surprises, no renegotiations, and no deals falling apart over a home inspection.

How to Read Long Island Real Estate Trends for Your Specific Situation

Generic market analysis won’t tell you what your home is worth or how quickly it will sell. Instead, here’s how to translate broad Long Island real estate trends into actionable intelligence for your situation.

Check hyper-local comparables

Rather than relying on county-level data, search recently sold homes within a half-mile radius of your property, in the same school district, of similar age, size, and condition, sold in the last 90 days. This gives you real pricing data, not theoretical market trends. For example, if you see homes similar to yours sitting for 120+ days, that’s your market reality—not what county-wide medians suggest. Resources like Redfin’s Long Island market data and Realtor.com’s market trends can provide baseline information, though local MLS data is most accurate.

Factor in your timeline urgency

Immediate need (0–30 days): traditional listings won’t work—therefore, you need cash buyers or investors willing to close fast. Learn more about how our process works and how we buy houses companies actually work. Moderate urgency (30–90 days): you might list traditionally if your home is updated and priced aggressively, but have a backup plan in case it doesn’t move. Compare cash buyer vs realtor options. Flexible timeline (90+ days): you can test the market, but watch holding costs carefully and understand the true cost of selling with a realtor.

Account for condition gaps

Long Island real estate trends heavily favor updated homes. As a result, if yours needs work: calculate realistic repair costs, subtract them from comparable prices, add your holding costs during renovations, then compare that number to a cash offer. Often, the cash offer nets more after accounting for time and expense. Many sellers wonder if cash home buyers pay fair prices—the answer depends on understanding why cash offers are lower and what you’re actually saving.

Understand seasonal patterns

Long Island markets still follow seasonal rhythms: spring (March–June) brings peak listing season with most buyers; summer slows slightly; fall (September–November) offers a second mini-peak; and winter is slowest but attracts serious buyers with less competition. If you’re in distress, however, waiting for the right season rarely makes financial sense—well-priced homes attract buyers year-round. See our complete guide to selling your house fast on Long Island for more detailed strategies.

Avoiding Cash Buyer Scams: Due Diligence Matters

With increased interest in fast home sales, understanding Long Island real estate trends also means knowing how to protect yourself. Not all cash buyers operate with the same integrity. Before accepting any cash offer, therefore, you should: verify the buyer has funds to close (proof of funds); check their business registration and reviews; understand all fees and closing costs; and get everything in writing.

Our guides on avoiding cash home buyer scams and whether we buy houses companies are legit can help you evaluate offers safely. In addition, knowing the key questions to ask any cash buyer before signing protects your interests. Our article on cash buyers vs wholesalers also explains who you’re actually dealing with.

The Property Father Difference: How We Work With Long Island Market Realities

Understanding Long Island real estate trends matters, but so does having a partner who can act on them quickly. At The Property Father, we’ve been buying homes in Nassau and Suffolk counties for years—through market peaks, valleys, and everything in between. As a result, we know which renovations buyers demand in Great Neck versus Patchogue. We understand how school district boundaries affect value in ways county-wide data doesn’t capture. And we’ve helped hundreds of distressed sellers navigate situations where market timing was a luxury they simply couldn’t afford.

We work in specific communities throughout Long Island, including Huntington, where we understand the unique market dynamics and buyer preferences.

Our Process: Simple, Transparent, Seller-First

First, you contact us by phone at (516) 548-6558 or through our contact page. From there, we evaluate your home remotely or in person, accounting for condition, location, and your timeline. Within 24 hours, you then receive a fair cash offer with no obligation to accept. After that, you choose your closing date—as fast as 7 days or as flexible as you need. We handle all closing costs and paperwork, making the process as straightforward as possible.

Unlike wholesalers, we’re not fishing for desperate sellers to flip. Instead, we buy homes to renovate and hold or rent. That means our offers reflect the true value of your property, not the lowest number we think you’ll accept. Understanding whether it’s worth selling your house for cash and the requirements for selling your house to a cash buyer therefore help set realistic expectations going in.

Making Your Decision: Speed, Price, or Certainty?

Long Island real estate trends in 2026 present choices, not guarantees. If you have time, money for repairs, and flexibility, a traditional listing might maximize your sale price. However, if you’re dealing with divorce, foreclosure, probate, or simply need to move on quickly, those trends matter far less than your immediate needs.

The right decision depends on three factors. First, your timeline urgency: do you need to close in weeks, or can you wait months for the right buyer? Second, your financial cushion: can you afford holding costs, repairs, and agent commissions—now typically around 5.5% combined and fully negotiable under the NAR settlement effective August 17, 2024—while you wait? Third, your stress tolerance: how much uncertainty, showing disruption, and negotiation can you realistically handle? Cash sales sacrifice some potential upside for certainty, speed, and simplicity. For many Long Island sellers in 2026, that trade-off makes perfect sense.

Ready to Sell Your Long Island Home Fast?

Understanding Long Island real estate trends helps, but at some point, analysis has to turn into action. Whether you’re navigating divorce, facing foreclosure, settling an estate, or simply ready to move on, The Property Father offers a straightforward alternative to the traditional listing process.

No repairs, no showings, and no waiting for buyer financing. Just a fair cash offer and a closing date that works for you.

For the complete guide on selling your Long Island home fast, see our comprehensive resource.

For additional insights and real estate tips, follow us on YouTube and Pinterest. Questions? Call (516) 548-6558 today.