Standing in your Long Island home looking at cracked foundation walls, an outdated kitchen, or a roof that’s seen better days, you’re facing one of the biggest questions in real estate: should I repair my house before selling, or just sell as-is and move on? The answer isn’t as simple as “always fix it” or “never spend a dime.” In 2026, Nassau and Suffolk County homeowners need to run the actual numbers — comparing repair costs, potential return on investment, time to recoup expenses, and the certainty of closing — before making this decision. What makes financial sense for a pristine home in Huntington might be completely wrong for an inherited property in Patchogue that needs extensive work.

Repair vs Sell As-Is

Real Cost Comparison

Scenario 1: Cosmetic ($19K)

Scenario 2: Major Systems ($32K)

Scenario 3: Foundation ($53K)

Repair ROI

Paint

Roof

Foundation

• Cosmetic (<$15K)

• Hot market

• Have time & cash

• Major (>$25K)

• No reserves

• Need speed

The Real Cost of Pre-Sale Repairs

Before you can decide whether to repair or sell as-is, you need to understand what repairs actually cost on Long Island — not national averages, but local contractor rates for 2026.

Major Repair Costs (Long Island, 2026)

Structural Issues:

- Foundation repair (cracks, settling): $5,000–$25,000+

- Structural beam replacement: $3,000–$10,000

- Major framing issues: $8,000–$30,000

Roof and Exterior:

- Full roof replacement (1,500–2,000 sq ft): $12,000–$20,000

- Roof repair (shingle replacement, flashing): $2,000–$5,000

- Siding replacement: $10,000–$25,000

- Window replacement (10–15 windows): $8,000–$15,000

Systems:

- HVAC replacement (furnace + AC): $8,000–$15,000

- Electrical panel upgrade: $2,500–$5,000

- Plumbing repairs (repiping sections): $3,000–$8,000

- Water heater replacement: $1,500–$3,000

Interior Updates:

- Kitchen renovation (mid-grade): $20,000–$50,000

- Bathroom renovation: $8,000–$20,000

- Flooring replacement (entire home): $8,000–$15,000

- Interior painting (whole house): $5,000–$10,000

Hidden Costs:

- Permits and inspections: $500–$2,000

- Project management and coordination: Your time (20–40 hours)

- Financing costs if you need to borrow: Interest on loans

- Carrying costs during repairs: Mortgage, taxes, insurance (3–6 months)

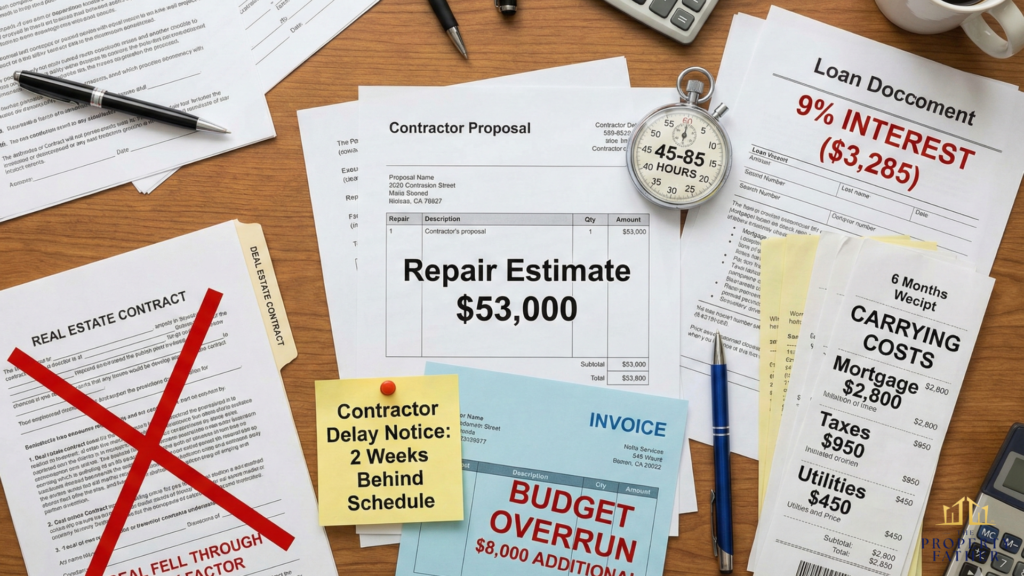

For a typical Long Island home needing moderate updates, you’re looking at $30,000–$75,000 in pre-sale repairs. Major renovations or structural issues can easily push costs over $100,000.I recoup these costs?”

Return on Investment: What Repairs Actually Pay Back

Industry data — particularly the annual 2025 Zonda/JLC Cost vs. Value Report, the authoritative benchmark for renovation ROI — shows that most pre-sale repairs don’t return 100% of their cost when you sell. Here’s what you can realistically expect on Long Island in 2026.

Advisory Note: ROI figures below are based on national averages from the 2025 Zonda/JLC Cost vs. Value Report and industry consensus data. Actual ROI varies by property, neighborhood, local market conditions, and scope of work. These figures are illustrative benchmarks, not guaranteed outcomes.

High-ROI Repairs (Strong return)

Fresh Paint: Cost: $5,000–$8,000 (whole house, professional) Return: Strong — widely cited as one of the highest-return cosmetic improvements for minimal investment Industry consensus supports fresh neutral paint as a strong performer because it improves showing quality and buyer perception at low cost relative to perceived value lift. A specific percentage ROI for interior painting is not tracked in the Cost vs. Value Report, but real estate professionals consistently rate it among the best pre-sale investments.

Minor Kitchen Updates: Cost: $5,000–$10,000 (new appliances, cabinet painting, countertops) Return: Approximately 113% (minor kitchen remodel, per the 2025 Zonda/JLC Cost vs. Value Report) Minor kitchen remodels — cabinet fronts, hardware updates, new appliances, fresh countertops — are among the strongest performers in 2025. Full renovation returns are far lower (see below).

Curb Appeal: Cost: $2,000–$5,000 (landscaping, power washing, minor repairs) Return: High — exterior projects dominate the top ROI rankings in 2025 Per the 2025 Cost vs. Value Report, specific curb appeal projects lead all categories: garage door replacement (approximately 194–268% ROI), steel entry door replacement (approximately 188–216%), and manufactured stone veneer (approximately 208%). General landscaping and power washing provide strong results at low cost.

Medium-ROI Repairs (Moderate return)

Bathroom Updates: Cost: $8,000–$15,000 (mid-range renovation) Return: Approximately 74–80% (midrange bathroom remodel, 2025 Zonda/JLC Cost vs. Value Report) Updating bathrooms improves showing quality and buyer confidence, but you won’t dollar-for-dollar recover the full cost unless the bathroom is truly non-functional.

HVAC Replacement: Cost: $8,000–$12,000 Return: Approximately 50–70% (industry consensus) Buyers expect working systems, but a new furnace or AC unit is viewed as a baseline necessity rather than an added amenity.

Flooring Replacement: Cost: $8,000–$12,000 (hardwood or quality laminate) Return: Approximately 70–80% (industry consensus) New floors improve showing quality but don’t recover their full cost in the sale price.

Lower-ROI Repairs (Modest return)

Major Kitchen Renovation: Cost: $30,000–$50,000 Return: Approximately 38–55% (2025 Zonda/JLC Cost vs. Value Report) A full kitchen gut-and-redesign is one of the weakest investments before a sale. You might spend $40,000 and see only $15,000–$22,000 in added sale price. Buyers have their own tastes and often plan to renovate themselves.

Roof Replacement: Cost: $15,000–$20,000 Return: Approximately 60–70% (industry consensus) Necessary to make the home marketable in many cases, but buyers treat a new roof as a corrected deficiency rather than a value-add. You’ll recoup roughly 60–70 cents on the dollar.

Foundation Repair: Cost: $15,000–$25,000 Return: Variable and difficult to quantify

Advisory Note: Foundation repair ROI is not tracked as a standard project in the Cost vs. Value Report because it varies enormously by severity, market, and buyer perception. Unlike kitchen or bathroom upgrades, foundation repairs eliminate a dealbreaker rather than add appeal — buyers typically view repairs as “finally fixed” rather than an improvement. In many cases, selling as-is to an investor makes more financial sense than funding structural repairs out of pocket.

The Math: Repair vs Sell As-Is Scenarios

The following three scenarios use illustrative numbers based on typical Long Island market conditions. Actual results vary by property, local market, time on market, negotiated sale price, and individual circumstances.

Advisory Note: Commission rates are fully negotiable and are not set by law. Following the August 2024 NAR settlement, sellers are no longer automatically required to pay the buyer’s agent commission. The 5.5% agent commission used in these scenarios reflects an estimated current rate for illustrative purposes only; actual rates in your transaction may be higher or lower.

Scenario 1: Minor Cosmetic Issues (Illustrative)

Property: $500,000 Long Island colonial, dated but functional Issues: Old carpet, 1980s kitchen, needs paint, minor repairs

Option A: Make Repairs

- Repairs needed: Painting ($6,000), new carpet ($5,000), minor kitchen update ($8,000)

- Total repair cost: $19,000

- Time to complete: 4–6 weeks

- Expected sale price: $515,000 (repairs increase value ~$15,000)

- Agent commission (estimated ~5.5%; fully negotiable): –$28,325

- Carrying costs during repairs/sale (4 months): –$10,000

- Net proceeds: $457,675

- Time to cash: 5–6 months

Option B: Sell As-Is to Cash Buyer

- Cash offer (as-is): $465,000

- No repairs needed: $0

- No commission: $0

- Carrying costs (2 weeks): –$600

- Attorney fees: –$2,000

- Net proceeds: $462,400

- Time to cash: 7–14 days

Result: Sell as-is nets approximately $4,725 more and closes 5 months faster in this scenario.

Scenario 2: Major Systems Need Replacement (Illustrative)

Property: $450,000 Long Island ranch, needs major work Issues: Roof needs replacement ($18,000), HVAC failing ($10,000), electrical panel upgrade needed ($4,000)

Option A: Make Repairs

- Repairs needed: $32,000

- Time to complete: 8–12 weeks

- Expected sale price: $470,000 (repairs increase value ~$20,000)

- Agent commission (estimated ~5.5%; fully negotiable): –$25,850

- Carrying costs (5 months): –$12,500

- Net proceeds: $399,650

- Time to cash: 6–7 months

Option B: Sell As-Is to Cash Buyer

- Cash offer (as-is): $395,000

- No repairs needed: $0

- No commission: $0

- Carrying costs (2 weeks): –$550

- Attorney fees: –$2,000

- Net proceeds: $392,450

- Time to cash: 7–14 days

Result: Repairs net approximately $7,200 more in this scenario — but require $32,000 in upfront capital and 6 months. For homeowners without cash reserves or time, selling as-is makes strong financial and practical sense.

Scenario 3: Foundation and Structural Issues (Illustrative)

Property: $425,000 Long Island Cape Cod, serious structural problems Issues: Foundation cracks ($20,000), structural repairs ($15,000), roof needs replacement ($18,000)

Option A: Make Repairs

- Repairs needed: $53,000

- Time to complete: 3–4 months (permits, inspections, contractor scheduling)

- Expected sale price: $445,000 (repairs increase value ~$20,000 due to market stigma on structural history)

- Agent commission (estimated ~5.5%; fully negotiable): –$24,475

- Carrying costs (6 months): –$15,000

- Net proceeds: $352,525

- Time to cash: 7–9 months

- Risk: Many traditional buyers still walk from homes with foundation repair history

Option B: Sell As-Is to Cash Buyer

- Cash offer (as-is): $365,000

- No repairs needed: $0

- No commission: $0

- Carrying costs (2 weeks): –$525

- Attorney fees: –$2,000

- Net proceeds: $362,475

- Time to cash: 7–14 days

- Certainty: Guaranteed close, no buyer backing out

Result: Sell as-is nets approximately $9,950 more than repairing and saves 7–8 months.

For detailed analysis of your options, see our Long Island home selling guide.

Hidden Costs of Making Repairs

The numbers above only show hard repair costs. Real-world repair projects come with hidden expenses that significantly impact your bottom line.

Time as a Cost

Managing contractors isn’t passive. You’ll spend:

- Getting quotes: 10–15 hours

- Researching and vetting contractors: 5–10 hours

- Project coordination: 20–40 hours

- Dealing with delays and issues: 10–20 hours

- Total: 45–85 hours of your time

If you’re employed, that’s 1–2 weeks of vacation time or weekends. If you’re relocating for work, coordinating from another state adds complexity and stress.

Carrying Costs During Repairs

While contractors work (typically 6–16 weeks), you’re paying:

- Mortgage: $2,500–$4,000/month

- Property taxes: $800–$1,200/month

- Insurance: $200–$300/month

- Utilities: $300–$500/month

Total carrying costs: $3,800–$6,000/month, or $23,000–$36,000 for a typical 6-month repair and sale timeline.

The Risk of Deals Falling Through

Even after repairs, traditional sales can and do collapse. According to Redfin’s 2025 contract cancellation data, approximately 13–15% of home purchase agreements are currently being canceled — a near-record level. Redfin’s survey of agents found that inspection and repair issues are the leading cause of cancellations, cited by 70.4% of agents who dealt with a cancellation, followed by buyer financing falling through (cited in approximately 28% of cases).

Separately, CoreLogic 2024 data shows appraisals came in below the purchase price in approximately 8.6% of transactions.

If your deal falls apart after 3 months in contract, you’re back to square one — having spent money on repairs with no sale. This risk is why many homeowners choose cash buyers with guaranteed closings over traditional sales.

Financing the Repairs

If you don’t have $30,000–$50,000 in cash reserves, you’ll need to:

- Take a personal loan (approximately 8–25%+ interest depending on creditworthiness)

- Use credit cards (18–25%+ interest)

- Get a home equity loan (approximately 8–10% interest, if you qualify)

Advisory Note: Loan rates vary significantly based on your credit profile, lender, and market conditions. Verify current rates with your lender before budgeting for repair financing. Interest costs can add $2,000–$5,000+ to repair expenses, further eroding ROI. Consult a licensed financial advisor before committing to a borrowing strategy.

Interest costs add materially to repair expenses, further eroding ROI.

When Repairs Make Financial Sense

Despite the costs, there are situations where investing in repairs before selling is the smart move.

You Should Make Repairs If:

- Your home is in a hot market with low inventory — When buyers are competing for homes in your neighborhood, well-presented properties get multiple offers above asking. The premium can justify repair costs.

- You have significant equity and time — If you own the home free and clear (or have minimal mortgage) and can wait 6–9 months, you can absorb carrying costs and work toward a higher sale price.

- The repairs are cosmetic and high-ROI — Fresh paint, new carpet, minor kitchen updates — if total costs are under $15,000 and expected ROI is strong (80%+), it can make sense.

- You can’t qualify for a cash sale offer — Some properties are in such poor condition that even investors won’t buy them. In rare cases, minimal repairs may be necessary to make the home sellable at all.

- You’re in Nassau County or Suffolk County neighborhoods where buyers expect turnkey — High-end areas command premium prices and buyers in those markets expect move-in ready homes. ROI may justify targeted renovations.

When Selling As-Is Makes More Sense

For many Long Island homeowners — especially those in difficult situations — selling as-is to a cash buyer is the financially superior choice.

Advisory Note: Selling as-is does not eliminate your disclosure obligations under New York law. Under New York Real Property Law §462 (amended March 20, 2024), sellers of residential real property must complete and deliver a mandatory Property Condition Disclosure Statement before the buyer signs a binding contract. The $500 opt-out credit that previously allowed sellers to skip the PCDS was eliminated effective March 20, 2024. Consult your attorney regarding your specific disclosure obligations.

You Should Sell As-Is If:

- Major systems need replacement — Roof, HVAC, foundation, electrical — when repair costs exceed $25,000 and ROI is 50–70%, you’re often better off selling as-is and letting the buyer factor repairs into the purchase price.

- You don’t have cash reserves for repairs — Borrowing money to fund repairs adds significant interest costs and reduces net proceeds. Cash buyers purchase without requiring any repairs.

- You’re facing foreclosure or need to sell quickly — When you have weeks, not months, repairs aren’t an option. Foreclosure situations require fast solutions.

- You’re dealing with inherited property or estate sales — Probate and inherited property situations often involve out-of-state heirs who can’t manage contractors across the country.

- You’re going through divorce — Selling during divorce is stressful enough without coordinating contractors and construction timelines.

- The property needs extensive work — When repair estimates exceed $50,000, traditional buyers will demand major concessions anyway. Cash buyers who specialize in these properties are often the most practical solution.

- You value certainty over maximum price — If avoiding financing-related deal collapses and guaranteeing a close date matter more than chasing an additional $10,000–$20,000, selling as-is provides that peace of mind.

Understanding how fast you can sell a house for cash helps you plan your timeline and make informed decisions.

The Hidden Value of Selling As-Is

Beyond avoiding repair costs, selling as-is to a cash buyer offers advantages that don’t show up in simple price comparisons.

Immediate Certainty

Cash buyers make offers within 24–48 hours and close in 7–14 days. You know exactly what you’re getting (no post-inspection price reductions), when you’re getting it (choose your closing date), and that the deal will close (no financing contingencies).

Zero Carrying Costs

Instead of paying $4,000–$6,000/month for 6–8 months during repairs and a traditional sale ($24,000–$48,000), you pay 2 weeks of carrying costs ($600–$1,200). The savings are significant.

No Sale Management Stress

Traditional sales require keeping the house showing-ready daily, accommodating showing schedules on short notice, managing multiple offers and negotiations, coordinating inspection repairs, dealing with appraisal issues, and watching for financing to fall through. An as-is cash sale requires one property visit, one offer review, and one closing.

Flexibility for Timing

Need to close before the holidays for estate distribution? Want to delay closing by 60 days to coordinate with a new purchase? Cash buyers accommodate your schedule in ways traditional buyers and agents typically cannot.

Common Mistakes Homeowners Make

Over-Improving for the Neighborhood: Installing $50,000 custom kitchens in middle-market neighborhoods that top out at $500,000 won’t deliver dollar-for-dollar returns. You can’t exceed the ceiling set by comparable sales.

Starting Repairs Without Getting Cash Offers First: Get a no-obligation cash offer before making any repair decisions. You might discover the as-is offer exceeds what you’d net after repairs and commissions — as the scenarios above show, this happens more often than most sellers expect.

Underestimating Repair Costs and Timelines: Contractors run over budget and behind schedule. Buffer your estimates by 30–40%. What you think costs $25,000 often becomes $35,000; an 8-week project often runs 14 weeks.

Ignoring Carrying Costs: Focusing only on repair costs while ignoring $5,000/month in mortgage, taxes, and insurance is a critical error. Carrying costs often exceed the difference between repairing and selling as-is.

Making Emotional Rather Than Financial Decisions: “I can’t sell my house like this” is emotional. “Will I net more money after repairs?” is financial. Run the actual numbers before deciding.

Not Understanding Market Preferences: Some Long Island neighborhoods want modern farmhouse kitchens. Others prefer traditional styles. Renovating based on HGTV trends rather than local buyer preferences wastes money.

Learning about when selling to investors makes sense helps you avoid these mistakes.

How to Decide: The Decision Framework

Step 1: Get Professional Estimates — Hire contractors to assess your property and provide written repair estimates. Don’t guess at costs.

Step 2: Research Comparable Sales — Look at recent sales in your neighborhood for similar homes in as-is condition and recently renovated homes, and note the price premium renovations actually commanded.

Then, Step 3: Calculate Your Repair ROI — Use this formula: (Expected Sale Price After Repairs – Repair Costs – Agent Commission – Carrying Costs) vs. Current As-Is Value

Step 4: Get a Cash Offer — Contact local cash buyers to receive as-is offers. This gives you a concrete baseline for comparison with no obligation.

Step 5: Consider Non-Financial Factors — Do you have time for a 6–9 month sale process? Can you manage contractors from your location? Do you have cash reserves? How important is closing certainty vs. maximum price?

Step 6: Run Multiple Scenarios — Calculate best-case (repairs go perfectly, home sells quickly) and worst-case (delays, cost overruns, deal falls through) outcomes.

Step 7: Make Your Decision — Choose the path that makes financial sense AND fits your situation, timeline, and stress tolerance.

Real Long Island Example: When As-Is Was Better

A Huntington homeowner inherited her parents’ 1960s ranch. The property needed roof replacement ($18,000), HVAC replacement ($12,000), kitchen and bath updates ($35,000), and cosmetic improvements ($8,000) — total repairs: $73,000.

Repair Option (Illustrative):

- Investment needed: $73,000 (borrowed at ~9% interest)

- Expected sale price: $525,000

- Agent commission (~5.5%, estimated; fully negotiable): –$28,875

- Carrying costs (6 months): –$18,000

- Interest on loan: –$3,285

- Net proceeds: $401,840

- Timeline: 7–9 months | Risk: traditional sale financing contingencies

As-Is Cash Sale:

- Cash offer: $415,000 | Investment needed: $0 | No commission: $0

- Carrying costs (2 weeks): –$700 | Attorney fees: –$2,000

- Net proceeds: $412,300

- Timeline: 10 days | Risk: Zero (guaranteed close)

By selling as-is, she netted approximately $10,460 more than the repair path — and closed in 10 days instead of 7–9 months. Understanding whether a cash sale is worth it comes down to running your specific numbers.

Ready to Sell Your Long Island Home Fast?

The question “should I repair house before selling” doesn’t have a universal answer. It depends on your repair costs, expected ROI, available cash, timeline, and personal circumstances. For many Long Island homeowners — especially those facing major repairs, tight timelines, or distress situations like foreclosure or divorce — selling as-is to a cash buyer delivers better financial outcomes with far less stress.

If repair costs are high, time is limited, or you simply want to avoid months of uncertainty, a cash offer might be your best path forward. Get a fair, no-obligation offer in 24 hours and close in as little as 7 days — no repairs, no showings, no risk.

See our Long Island Home Selling Guide for a complete breakdown of your options.