“We buy houses for cash!” appears on signs, websites, and mailers throughout Nassau and Suffolk County. But not all companies claiming to be cash buyers actually purchase properties. Understanding the cash buyer vs. wholesaler difference protects Long Island homeowners from transactions that look secure but deliver uncertainty, last-minute price reductions, and potential deal collapse.

In 2026, wholesalers have become increasingly sophisticated in presenting themselves as legitimate cash buyers. They use professional websites, polished marketing materials, and language suggesting they’re purchasing your property directly. In reality, they’re contract flippers—middlemen who never intend to buy your home but instead market your property to actual investors, pocketing the difference between their contract price and what end buyers will pay.

This article exposes the wholesaling business model, explains how it creates risks for sellers, reveals the telltale signs that identify wholesalers, and demonstrates how The Property Father operates differently as an actual purchaser with capital, capability, and commitment to close every transaction we offer on. The goal isn’t to vilify wholesaling as a business model—it’s to ensure you understand what you’re agreeing to and can make informed decisions about who you work with.

Actual Buyer vs Wholesaler

Know the Critical Difference

✓ Actual Buyer

Timeline: 7-14 days

Contract: Direct purchase

Certainty: 98% close rate

Price: Firm offer honored

Business: Owns properties

Risk: Minimal to none

✗ Wholesaler

Timeline: 45-60+ days

Contract: “And/or assigns”

Certainty: 40% fail rate

Price: Often renegotiated

Business: Flips contracts

Risk: High deal collapse

How Wholesaling Works

2. Find actual buyer ($370K)

3. Assign contract, keep difference ($30K)

4. Deal fails if no buyer found

🚨 Wholesaler Red Flags

• Won’t show proof of funds

• “Subject to partner approval”

• Long inspection periods (30+ days)

• Vague about business model

• Extended closing timelines

✓ Property Father Guarantee

• Immediate proof of funds

• Firm 7-14 day closing

• No price renegotiation

• 300+ completed purchases

• 98% close rate (8 years)

What Wholesaling Actually Is

Before examining problems, understanding the wholesaling business model reveals why it creates seller risks.

The Wholesaling Business Model

Wholesalers operate as middlemen in real estate transactions:

1. Contract your property

- Wholesaler offers to purchase your home

- You sign purchase contract giving them right to buy

- Contract includes “and/or assigns” or “assignee” language

- No money changes hands (or minimal earnest deposit)

2. Market your property to actual buyers

- Wholesaler emails your property to investor buyer lists

- Advertises on investor forums and websites

- Shops your property to multiple potential buyers

- Negotiates with investors while you wait

3. Assign contract to end buyer

- Wholesaler finds investor willing to pay more than contract price

- “Assigns” the purchase contract to that investor

- Wholesaler keeps the difference as “assignment fee”

- End buyer actually purchases your property

Wholesaling is a legal business model in New York when conducted properly. Under New York Real Property Law Article 12-A, unlicensed wholesalers may not market the property itself—they may only market their equitable interest in the purchase contract. Wholesalers who publicly advertise or broker the sale of the property without a license may be acting outside the bounds of New York law. Understanding how we buy houses companies work helps you distinguish between different types of operators. The problems for sellers arise when wholesalers misrepresent themselves as direct buyers and when deals fail to materialize.

Example Wholesaling Transaction

Your situation: Home worth $450,000 retail, needs $40,000 repairs

Wholesaler’s approach:

- Offers $340,000 cash purchase

- You sign contract believing they’re buying

- Contract says “ABC Company and/or assigns”

Behind the scenes:

- Wholesaler markets to investors at $365,000–$375,000

- Finds buyer willing to pay $370,000

- Wholesaler assigns contract, keeping $30,000 difference

- End buyer actually purchases your property for $340,000

Your experience:

- Different buyer shows up at closing than you contracted with

- You receive $340,000 as contracted

- Never know wholesaler made $30,000 on the transaction

- Deal could have collapsed if wholesaler couldn’t find buyer

The transaction closed, but involved uncertainty and a middleman you didn’t need.

Why Wholesalers Present as Cash Buyers

Wholesalers benefit from appearing to be direct buyers:

- Seller cooperation: Homeowners more readily work with buyers than middlemen

- Contract signing: Easier to get signatures if sellers believe buyer has funds

- Time: Prevents sellers from shopping other offers while wholesaler finds buyers

- Pricing: Can negotiate lower prices by implying direct purchase certainty

Understanding the cash buyer vs. wholesaler difference helps you distinguish between actual purchasers and contract flippers.contract flippers.

The Problems Wholesaling Creates for Sellers

Wholesaling introduces risks that working with actual cash buyers eliminates.

Problem 1: No Guarantee of Closing

Wholesaling introduces risks that working with actual cash buyers eliminates.

Problem 1: No Guarantee of Closing

The fundamental issue: wholesalers don’t have funds to close and only complete transactions if they find end buyers.

What happens when wholesalers can’t find buyers:

- Contract expires without closing

- You’ve wasted 30–60 days off-market

- Must restart entire selling process

- Property has aged, possibly requiring price reductions

- Lost opportunity to work with actual buyers

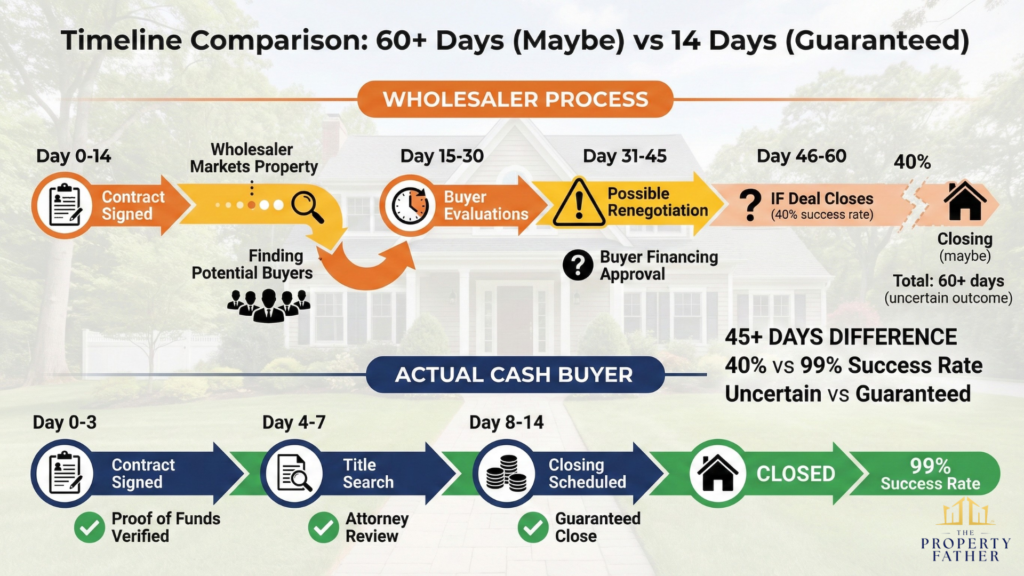

Advisory Note: No verified primary source exists for a specific wholesaler contract failure rate. The risk of non-closure is a well-documented industry concern, but published data on contract cancellations covers all real estate transactions broadly. According to Redfin’s 2025 analysis, Nassau County, NY has one of the lower overall contract cancellation rates among major metros (approximately 6.8%). Wholesaler-specific failure rates are higher than typical buyer transactions because of their reliance on finding end buyers, but sellers should not rely on any specific percentage without consulting local real estate professionals familiar with the current market.

Representative scenario: A Nassau County seller contracts with a wholesaler at $375,000. After 45 days, the wholesaler cannot find a buyer and the contract expires. The seller has turned away other offers during that period and eventually sells to an actual investor for $365,000—$10,000 less after losing six weeks.

Problem 2: Last-Minute Price Reductions

Wholesalers frequently renegotiate prices downward when their investors demand it.

Common scenarios:

“Inspection revealed issues” (that existed all along)

- Wholesaler’s end buyer wants lower price

- Wholesaler blames “newly discovered” problems

- Pressures you to reduce price to save the deal

- You’re in weak position after waiting weeks

“Market changed”

- Wholesaler can’t find buyer at original price

- Claims market conditions shifted

- Demands price reduction as only way to close

- You’ve stopped marketing to alternatives

“Financing complications”

- End buyer’s financing fell through

- New buyer needs lower price

- Wholesaler presents as your only option

- Accept reduction or start over

Advisory Note: The range of $10,000–$30,000 below original contract price is an illustrative industry-observed range, not a data-sourced average. Actual renegotiation amounts vary significantly by property value, market conditions, and individual operator. Confirm current conditions with a licensed New York real estate attorney before making decisions based on these estimates.

These tactics leave sellers accepting prices below their original contracts, after already losing time and alternatives.

Problem 3: Extended Timelines

Wholesalers need time to find buyers, creating delays actual cash buyers don’t have.

Typical wholesaler timeline:

- Contract signing: Day 0

- Marketing to buyers: Days 1–14

- Buyer evaluation period: Days 15–28

- Buyer financing/approvals: Days 29–60

- Closing: Days 60–75 (if it happens)

Compare to actual cash buyer: 7–21 days total in New York, depending on title and attorney scheduling.

For sellers facing foreclosure, divorce, or job relocation, these delays create serious problems.

Problem 4: No Proof of Funds

Because wholesalers don’t intend to purchase themselves, they can’t provide legitimate proof of funds.

What wholesalers do instead:

- Refuse to provide proof of funds

- Show minimal earnest money deposit only

- Claim “our investors provide the funding”

- Deflect questions about financial capability

- Rely on contract contingencies as escape routes

Without proof of funds, you have no verification they can close—because they can’t. Their ability to close depends entirely on finding qualified buyers.

Problem 5: Reduced Negotiating Power

Working through wholesalers weakens your position.

Direct to investor:

- You negotiate directly with buyer making final decision

- Can address concerns and objections immediately

- Build relationship with actual purchaser

- Understand real buyer’s motivations and constraints

Through wholesaler:

- Wholesaler controls communication with end buyers

- Your concerns filtered through middleman

- Don’t know actual buyer’s capabilities or timeline

- Wholesaler’s profit margin takes priority over your interests

This distance costs sellers both money and favorable terms.

How to Identify Wholesalers

Specific warning signs reveal when you’re dealing with contract flippers rather than actual buyers.

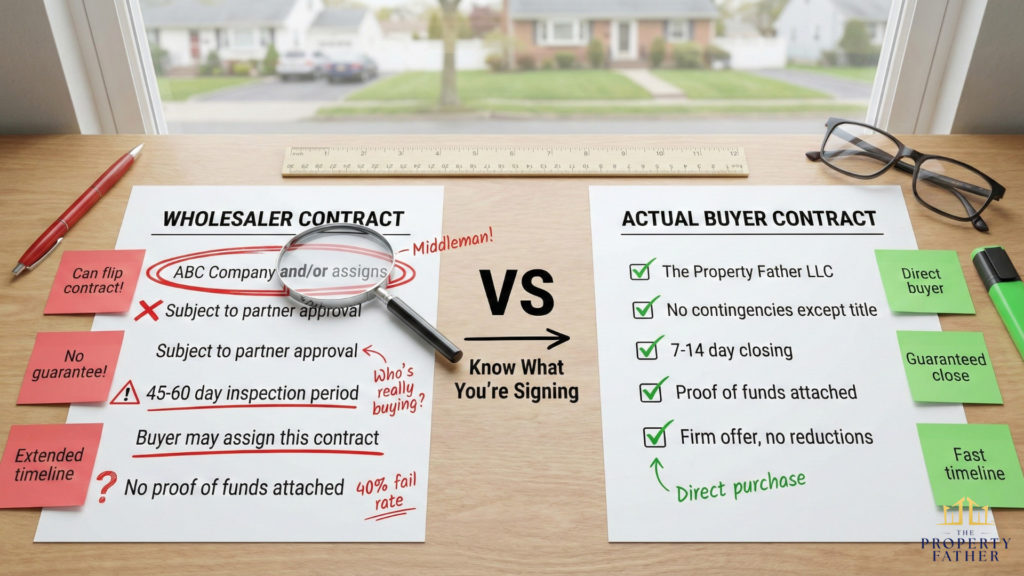

Red Flag 1: Contract Language

Wholesaler indicators:

- “ABC Company and/or assigns” as buyer name

- “Buyer reserves the right to assign this contract”

- “Subject to partner approval” clauses

- “This agreement is assignable” language

Actual buyer language:

- Company name only (no “and/or assigns”)

- Direct purchase by named entity

- No assignment provisions

- No partner approval contingencies

New York real estate contracts from actual buyers name the purchasing entity directly without assignment loopholes.

Red Flag 2: No Proof of Funds

Wholesaler behavior:

- Refuses to provide bank statements

- Shows only minimal earnest deposit

- Can’t produce pre-approval letters

- Claims “funding comes later”

- Becomes evasive when pressed

Actual buyer behavior:

- Provides bank statements immediately

- Shows accounts with sufficient funds

- Pre-approval letters from lenders (if financing)

- Financial documentation current (within 30 days)

- Welcomes verification with banks

If someone claiming to buy your home won’t prove they have funds, they’re not actually buying—they’re wholesaling.

Red Flag 3: Extended Inspection Periods

Wholesaler contracts:

- 14–30 day inspection periods (need time to find buyers)

- Vague inspection language allowing subjective outs

- “Subject to satisfactory inspection” without specifics

- Long due diligence periods before earnest money at risk

Actual buyer contracts:

- Minimal or no inspection period (evaluated pre-offer)

- Buy properties as-is without inspection contingencies

- Quick timelines (7–21 days) don’t allow extended evaluation

- Earnest money at risk immediately

Legitimate cash buyers inspect before making offers. Wholesalers need long inspection periods to market properties.

Red Flag 4: Questions About Your Timeline Flexibility

Wholesaler focus:

- “Can you wait 45–60 days to close?”

- “Would you be flexible if we need more time?”

- “We might need to extend the contract”

- Emphasis on your patience and flexibility

Actual buyer focus:

- “When do you need to close?”

- “We can close as quickly as you need”

- “7–14 days works for us—does that fit your timeline?”

- Accommodating your needs, not theirs

Wholesalers need time to find buyers. Actual buyers have funds ready and close on your schedule.

Red Flag 5: Vague About Their Business Model

Wholesaler responses:

- “We work with a network of investors”

- “Our partners provide the capital”

- “We coordinate real estate transactions”

- Avoids direct answers about how they operate

Actual buyer responses:

- “We purchase properties directly and renovate them”

- “Our company owns the properties we buy”

- “We’re investors who buy, fix, and resell”

- Clear, direct explanation of business model

Ask directly: “Are you the actual buyer, or will you assign this contract?” Their answer reveals everything.

How The Property Father Operates Differently

Understanding our business model shows why working with actual buyers benefits sellers.

We Are the Buyer

Our commitment:

- The Property Father purchases every property we contract

- Our company name appears as buyer (no “and/or assigns”)

- We close in our name and hold properties during renovation

- No contract assignment or flipping to other buyers

What this means for you:

- Person making offer is person closing deal

- No surprise buyer showing up at closing

- Relationship with decision-maker throughout process

- Direct communication without middlemen

When we make offers, we’re committing to purchase—not looking for permission to find someone else who will.

We Provide Immediate Proof of Funds

Our standard practice:

- Bank statements provided within 24 hours of request

- Current statements (within 30 days) showing liquid capital

- Pre-approval letters from lenders for larger acquisitions

- Previous closing statements demonstrating track record

Verification encouraged:

- Call our bank directly to verify accounts

- Contact our attorney to confirm closing capability

- Review our purchase history through public property records

- Speak with past sellers about our reliability

We welcome verification because we have nothing to hide.

Our Contracts Are Clean and Direct

The Property Father contract terms:

- Company name only as buyer (no assignment language)

- No partner approval contingencies

- Minimal contingencies (title only—standard for all sales)

- Firm closing timeline (7–21 days typical)

- No extended inspection periods for finding buyers

What you won’t see:

- “And/or assigns”

- “Subject to partner approval”

- “Right to assign this agreement”

- Vague satisfaction clauses

- Long due diligence periods

Our contracts reflect actual purchase intent because we’re buying, not flipping contracts.

We Close on Your Timeline

Our flexibility:

- 7–14 days standard (we’re ready when you are)

- Can close faster if you need

- Can accommodate delays if you need more time

- Work around your schedule, not ours

Why we’re flexible:

- Our funds are available immediately

- No need to find buyers or arrange financing

- No partners requiring approval or coordination

- Direct decision-making allows quick responses

Actual buyers with capital can accommodate seller timelines. Wholesalers need time to find buyers and can’t guarantee flexibility.

We Honor Our Offers

Our commitment:

- Written offers are firm based on property condition as represented

- No price reductions except undisclosed issues or title problems

- No “inspection discoveries” of problems we already knew about

- No market condition excuses for renegotiation

Advisory Note: The specific close rate, timeline, and performance figures cited in this section reflect Property Father’s self-reported operating history. Prospective sellers are encouraged to independently verify these claims through public property records, BBB, Google reviews, and direct reference checks before making decisions based on them.through reputation and reliability.

Real Cost Comparison: Wholesaler vs. Actual Buyer

The difference isn’t just operational—it affects your net proceeds and timeline.

Scenario: $450,000 Retail Value Home

Advisory Note: The figures in this comparison are illustrative scenarios, not data-sourced averages. Actual offers, failure rates, timelines, and net proceeds vary significantly by property condition, local market conditions, and individual buyer or wholesaler. Consult a licensed New York real estate attorney and consider multiple offers before making decisions.

Wholesaler approach:

- Offer: ~$345,000

- Timeline: 45–60 days (if it closes at all)

- Risk of deal collapse: Meaningful — dependent on finding an end buyer

- Risk of price reduction: Common in wholesaler transactions per industry reporting

- Net proceeds: Uncertain — could be reduced from original contract price

The Property Father approach:

- Offer: ~$340,000

- Timeline: 7–14 days

- Risk of deal collapse: Minimal (title issues only)

- Risk of price reduction: Not our practice

- Net proceeds: Equal to contracted price

Analysis: Our illustrative offer is nominally lower, but it is guaranteed and certain. The value of certainty — particularly for sellers in time-sensitive situations like foreclosure, divorce, or estate settlement — can far exceed a modest difference in gross offer price when the alternative carries real risk of deal collapse and renegotiation.

Understanding whether cash offers are fair requires looking beyond gross numbers to certainty and net proceeds.

Questions That Expose Wholesalers

Use these specific questions to determine if you’re working with actual buyers or contract flippers.

Question 1: “Can you show me proof of funds today?”

- Actual buyer response: “Absolutely—I’ll email bank statements within the hour”

- Wholesaler response: Delays, excuses, or “our investors provide funding”

Question 2: “Will your company name appear as buyer on the contract?”

- Actual buyer response: “Yes—The Property Father is the purchasing entity”

- Wholesaler response: “We might assign to partners” or contract includes “and/or assigns”

Then, Question 3: “Have you personally purchased properties, or do you assign contracts?”

- Actual buyer response: “We purchase directly—I can show you properties we own”

- Wholesaler response: Evasive answer about “working with investors”

Question 4: “What contingencies does your offer include?”

- Actual buyer response: “Only title—standard for all purchases”

- Wholesaler response: Inspection contingencies, financing, partner approval

Question 5: “How many properties have you personally purchased in the last year?”

- Actual buyer response: “We’ve closed on 40+ Long Island properties”

- Wholesaler response: Can’t provide specific number or shows few closings

Learning what questions to ask cash buyers protects you from wholesaler pitfalls.

When Wholesaling Might Work (Rare Cases)

Fairness requires acknowledging situations where wholesaling could be acceptable.

Acceptable Wholesaler Scenarios

1. Full disclosure upfront

- Wholesaler clearly states they’re flipping contracts

- Explains their business model transparently

- Doesn’t misrepresent as direct buyer

- You accept this knowing the risks

2. You have extended timeline

- No urgency to close quickly

- Can afford 60–90 day marketing period

- Don’t mind potential renegotiation

- Willing to accept deal collapse risk

3. Property has unusual challenges

- Requires very specific buyer (unusual property)

- Wholesaler has connections to niche buyers

- Direct buyers have passed on property

- Wholesaler’s network provides value

4. You maintain leverage

- Continue marketing to other buyers during contract period

- Short inspection period limits wholesaler time

- Strong contract terms protect against renegotiation

- Attorney carefully reviews assignment provisions

Even in these cases, working with actual buyers typically delivers superior outcomes. But informed sellers making conscious choices to work with disclosed wholesalers isn’t problematic—it’s the misrepresentation that creates issues. You can evaluate whether selling for cash is worth it based on your specific situation.

How to Protect Yourself

If You’ve Signed with a Wholesaler

- Review your contract immediately with a real estate attorney

- Request proof of funds in writing

- Clarify assignment rights and whether contract can be flipped

- Set firm deadlines for their performance

- Continue marketing to backup buyers if contract allows

- Don’t agree to price reductions without documented justification

- Walk away if red flags appear before it’s too late

When Evaluating Any “Cash Buyer”

- Ask directly: “Are you the actual buyer or will you assign this?”

- Demand proof of funds immediately

- Review contracts for assignment language

- Check their purchase history through public property records

- Speak with past sellers about their experience

- Compare multiple offers from different buyers

- Have attorney review before signing anything

Understanding how to avoid cash buyer scams includes recognizing wholesaler tactics.

The Property Father’s Commitment

We operate as actual buyers because it’s the right way to serve Long Island homeowners.

Our Operating Principles

- Transparency: We explain our business model clearly—we buy, renovate, resell

- Capital: We maintain funds to purchase every property we offer on

- Commitment: Our offers are firm commitments, not fishing expeditions

- Speed: We close in 7–14 days because we’re ready to purchase

- Honoring agreements: We close at contracted prices unless title issues arise

Why We Don’t Wholesale

We could make faster money flipping contracts without capital investment. We choose not to because:

- Seller uncertainty — Wholesaling creates risks for people who deserve better

- Reputation — Long-term business requires trust and reliability

- Control — Direct ownership allows quality renovations benefiting neighborhoods

- Relationships — We build lasting connections with sellers, contractors, and community

Our business model requires more capital and longer holding periods, but delivers better outcomes for everyone involved.everyone involved.

Ready to Sell Your Long Island Home?

Understanding the cash buyer vs wholesaler difference protects you from transaction uncertainty, last-minute price reductions, and potential deal collapse. Wholesalers serve a role in real estate markets, but sellers deserve to know who they’re working with and what risks they’re accepting.

The Property Father operates as an actual purchaser with proven capital, closing capability, and commitment to honor every offer we make. We provide immediate proof of funds, use clean contracts without assignment clauses, close in 7-14 days on your schedule, and have completed 300+ Long Island purchases over 8 years.

Get a guaranteed offer from an actual buyer in 24 hours. We’ll prove our funds, explain our offer calculation, accommodate your timeline, and close at the contracted price—no surprises, no renegotiations, no contract flipping.

See our Long Island Home Selling Guide for a complete breakdown of your options.