Selling your Long Island home to a cash buyer should feel like relief—fast closing, no repairs, no uncertainty. But for every legitimate investor providing valuable services, predatory operators exploit homeowners in vulnerable situations. Learning which cash home buyer scams to avoid protects your largest asset from theft disguised as a fair transaction.

In 2026, scammers have become increasingly sophisticated, using professional-looking websites, polished marketing, and pressure tactics that manipulate desperate homeowners into signing away equity. Nassau and Suffolk County residents facing foreclosure on Long Island, divorce, or inherited property challenges are particularly vulnerable to these schemes.

This article reveals five critical red flags that signal danger when dealing with cash buyers. Recognizing even one of these warning signs should make you pause, seek legal counsel, and likely walk away. Your home represents years of equity—protecting it requires knowing exactly what legitimate buyers never do.

⚠️ 5 Critical Red Flags

Cash Home Buyer Scams to Avoid

Demanding Immediate Signature

“Offer expires in 24 hours” • “Sign now or we move on” • Creating false urgency to prevent due diligence

Requesting Upfront Fees

Inspection fees • Processing fees • Any payment before closing • Legitimate buyers never charge sellers

No Proof of Funds

Refusing bank statements • Delaying financial verification • Can’t prove ability to close • Always demand immediate proof

Contingent Contracts

“Subject to partner approval” • “And/or assigns” language • Escape clauses • Real buyers use clean contracts

Discouraging Legal Review

“Attorneys slow things down” • “Simple contract, no need” • Preventing attorney involvement • Always use your own lawyer

✓ Protect Yourself

• Demand proof of funds immediately

• Hire independent attorney

• Never pay upfront fees

• Take time to review (5-7 days)

• Walk away from any red flag

Red Flag #1: Demanding Immediate Signature or Creating False Urgency

Legitimate business doesn’t require snap decisions on your largest financial asset.

The Pressure Tactic

Scam operators create artificial urgency designed to prevent you from thinking clearly, consulting advisors, or comparing offers. Common pressure tactics include:

“This offer expires in 24 hours.” Professional buyers typically provide offers valid for at least 5–7 days. Your property won’t suddenly lose value overnight, and legitimate buyers understand you need time for due diligence.

“Sign now or we move to the next house.” This manufactured scarcity implies other sellers are competing for their attention. Professional investors don’t pit desperate homeowners against each other.

“The market is crashing—sell before you lose everything.” Fear-based manipulation preys on anxiety about property values. According to the FHFA House Price Index, sustainable markets don’t collapse overnight, and legitimate buyers don’t profit from scaring you. For current Long Island market conditions, consult the most recent FHFA HPI data or your local MLS.

“Our funding expires at midnight.” Cash buyers with legitimate funding don’t face arbitrary deadlines. This creates panic to prevent you from verifying their claims.

Why They Use Pressure

Speed prevents you from:

- Getting competing offers from other buyers

- Consulting with real estate attorneys

- Researching their company’s history and reputation

- Discovering their offer is significantly below fair market value

- Realizing contract terms heavily favor them

What Legitimate Buyers Do Instead

Professional investors:

- Provide written offers valid for 5–7 days, giving you adequate time for due diligence

- Encourage you to get multiple offers for comparison

- Insist you consult with real estate attorneys

- Answer questions patiently without pressure

- Allow you to review offers with family members

When evaluating whether cash buyers are legitimate, patience and transparency distinguish professionals from predators.

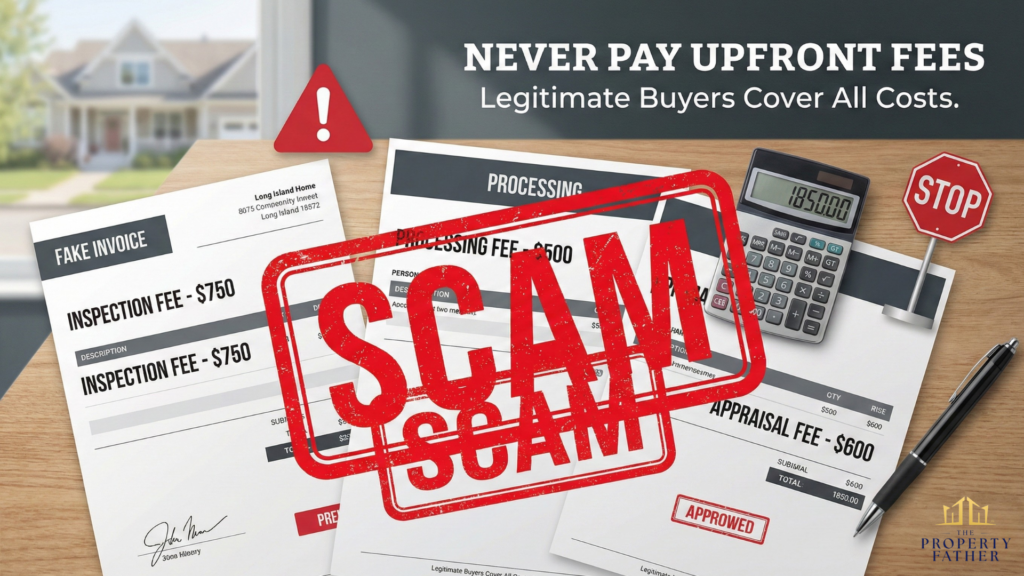

Red Flag #2: Requesting Any Upfront Fees or Payments

Legitimate cash buyers never ask sellers to pay anything before closing.

Common Fee Scams

“Property inspection fee.” Scammers request $300–$800 for “professional property evaluation” before making an offer. They either disappear with your money or provide lowball offers designed to be rejected, keeping your fee either way.

Real cash buyers absorb inspection costs as part of their business model. They make money buying and selling properties, not charging desperate sellers fees.

“Processing fee” or “paperwork fee.” Operators claim they need $200–$500 to “process your application” or “prepare closing documents.” The Federal Trade Commission identifies upfront fee requests in real estate transactions as a major warning sign of fraud.

Legitimate transaction costs — including your attorney’s fees, title search, and New York State transfer tax (0.4% of the sale price, typically paid by the seller under NY Tax Law §1402) — are paid at closing from sale proceeds, not upfront from your pocket.

Advisory Note: Closing costs vary by sale price, outstanding liens, and individual circumstances. Consult a licensed real estate attorney for a precise estimate before agreeing to any transaction terms.

“Appraisal fee.” Cash buyers arrange and pay for property valuations themselves. Any request for you to pay appraisal fees before receiving an offer indicates fraud.

“Contract review fee.” Your attorney reviews contracts as part of their closing services. Cash buyers never charge you to review their own contracts.

The Bait-and-Switch Variation

Some scammers advertise “no fees” but bury charges in contracts:

- “Assignment fees” paid to them at closing

- “Marketing costs” deducted from proceeds

- “Transaction coordination fees” reducing your net

- “Consultant fees” for their “services”

These hidden costs don’t appear until closing statements, catching sellers by surprise when it’s too late to back out without losing earnest money deposits.

Protection Strategy

Never pay anything upfront. If a cash buyer requests any payment before closing, walk away immediately. Legitimate investors covering evaluation costs themselves demonstrate they’re serious buyers with actual capital.

Understanding how legitimate cash buyers work reveals that professional operations never burden sellers with fees.

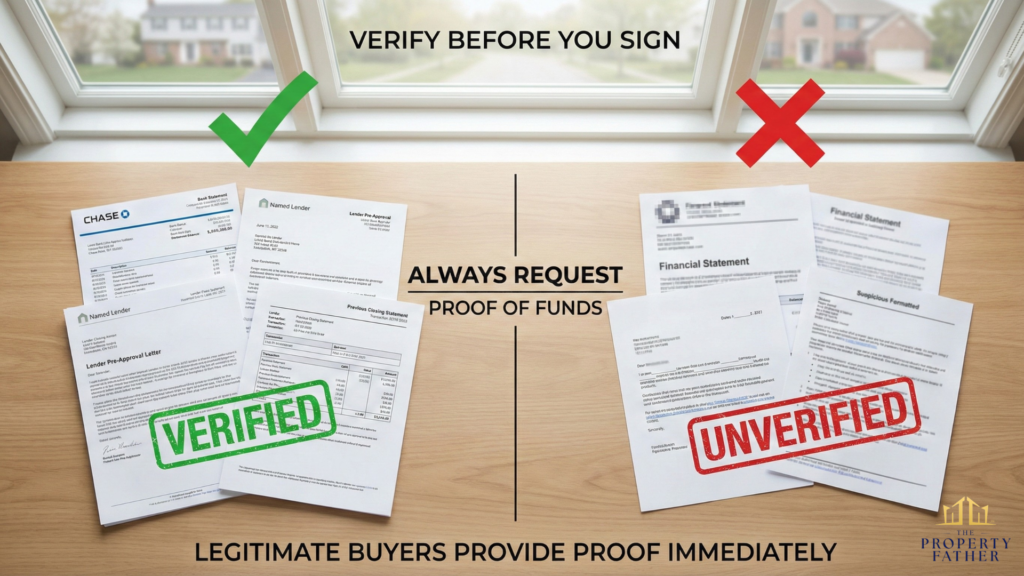

Red Flag #3: Refusing to Provide Proof of Funds

Anyone claiming to buy your house with cash must prove they actually have cash.

Why Proof Matters

Proof of funds documentation shows the buyer can close the transaction. Without it, you’re wasting time with someone who cannot fulfill their promises. For Long Island properties — where recent market data has put median values well above $400,000 (verify current figures via OneKey MLS or NAR) — buyers need substantial capital or financing in place.

What Legitimate Proof Looks Like

Bank statements showing account balances sufficient to cover the purchase price. These should be:

- Recent (within 30 days)

- From recognized financial institutions

- Showing liquid funds, not just lines of credit

- In the buyer’s or their company’s name

Pre-approval letters from lenders for investors using financing rather than pure cash. These specify:

- Approval amount covering your purchase price

- Property address or “to be determined”

- Expiration date showing current validity

- Lender contact information you can verify

Previous closing statements proving they’ve completed recent purchases. These demonstrate:

- Track record of actual closed transactions

- Ability to follow through on offers

- Experience buying properties like yours

Verification Steps

Don’t just accept documents at face value:

- Call the bank or lender directly using phone numbers from their official websites — not numbers on provided documents

- Request transaction references from their last 3–5 purchases with seller contact information

- Verify company ownership of accounts through business registration documents

- Check public records showing their recent property purchases in Nassau or Suffolk County

Red Flags in Responses

“We’re a private company — we don’t share financial details.” Private companies buying your home must still prove they can close. Privacy doesn’t override basic due diligence.

“Our funds are in escrow — you’ll see them at closing.” You see proof before accepting offers, not at closing when it’s too late to back out.

“We use partners who provide funding later.” This indicates wholesaling, not actual buying. Understanding the difference between cash buyers and wholesalers protects you from assignment schemes.

“Our attorney will provide proof.” Legitimate buyers provide proof directly, immediately, without involving third parties as intermediaries.

Red Flag #4: Using Contracts with Escape Clauses or Contingencies

Cash sale certainty is the primary value proposition. Contingent contracts defeat this purpose.

Problematic Contract Language

“Subject to partner approval.” This allows buyers to back out at any time by claiming their “partners” rejected the deal. You have no control over unknown partners’ decisions, leaving you in limbo.

“Subject to satisfactory inspection.” While seemingly reasonable, this gives buyers broad power to renegotiate or cancel after you’ve signed. They can claim any minor issue as “unsatisfactory” to force price reductions or walk away. Legitimate cash buyers conduct their assessments before making offers, not after you’ve committed.

“Subject to obtaining financing.” If they’re claiming to be “cash” buyers but their contracts require loan approval, they’re not actually cash buyers. Financing contingencies introduce all the uncertainty you’re trying to avoid.

“Buyer reserves the right to assign this contract.” This is wholesaler language, allowing them to flip your contract to another buyer. Assignment clauses are legal under New York real estate law, but their presence signals you’re dealing with a middleman — not a direct purchaser committed to closing the deal themselves.

What Legitimate Contracts Contain

Professional investor contracts include:

- Company name as direct buyer (not “and/or assigns”)

- Purchase price clearly stated without reduction mechanisms

- Specific closing date within 7–14 days

- Only a standard title contingency (ensuring you can legally transfer ownership)

- No financing contingency

- No partner approval requirement

- No vague “satisfaction” clauses

Your attorney should review all contracts, but clean language without escape hatches indicates a legitimate buyer committed to closing.

Why Contingencies Benefit Scammers

Escape clauses allow operators to:

- Lock up your property while marketing it to real buyers

- Renegotiate dramatically lower prices after you’ve stopped marketing to others

- Abandon the deal without penalty if they find better opportunities

- Pressure you into accepting reduced terms under time pressure

- Control your property without risking their own capital

When comparing your cash buyer vs. realtor options, contract terms matter as much as the offered price.

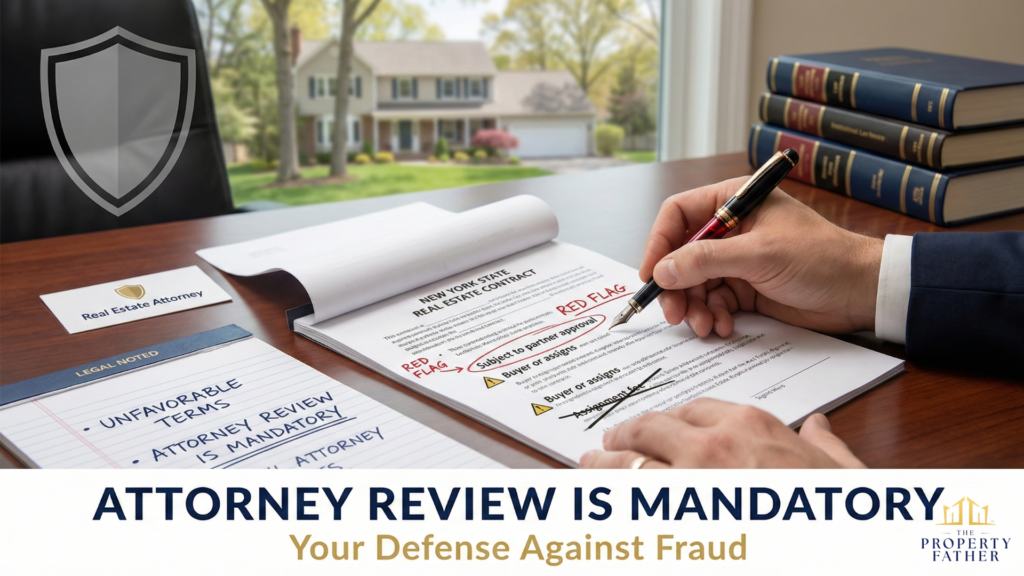

Red Flag #5: Discouraging or Preventing Legal Representation

Any buyer suggesting you don’t need an attorney is trying to take advantage of you.

Attorney Avoidance Tactics

“Attorneys just slow things down and cost money.” New York is an attorney-closing state, meaning legal counsel is standard practice in all residential real estate transactions. Legitimate buyers insist you have legal representation because it protects both parties and ensures proper documentation. Professional investors know that experienced attorneys catch contract problems that protect sellers. Only scammers fear attorney scrutiny.

“Our contracts are simple — you don’t need legal review.” Even “simple” contracts transferring property worth hundreds of thousands of dollars require attorney review. The New York State Bar Association and standard New York real estate closing practice both support attorney involvement in all transactions, regardless of complexity. Protecting your interests — not the contract’s length — is what matters.

“We’ll pay for your attorney if you use our recommended lawyer.” This creates a conflict of interest. Attorneys paid by buyers may prioritize buyer interests over yours. Always hire your own independent attorney.

“Sign now; you can have an attorney review later.” Reviewing contracts after signature is worthless. You’re already bound to terms. Attorneys must review before you sign, without exception.

Why Scammers Avoid Attorneys

Experienced real estate attorneys immediately recognize:

- Hidden fees and unfavorable terms

- Escape clauses favoring buyers

- Assignment language indicating wholesaling

- Below-market pricing suggesting equity theft

- Pressure tactics and fraudulent representations

- Title issues or clouds the buyer is exploiting

Attorneys ask questions scammers don’t want to answer and demand changes scammers don’t want to make.

What Legitimate Buyers Require

Professional cash buyers:

- Insist you retain independent legal counsel

- Provide adequate time for attorney review (3–5 days minimum)

- Answer attorney questions directly and honestly

- Welcome attorney involvement as transaction protection

- Use standard New York real estate contracts attorneys recognize

- Have their own attorneys coordinate with yours

When selling to legitimate Long Island cash buyers, attorney involvement is mandatory, not optional.

Protection Strategy

Always hire your own real estate attorney before signing anything. Never use buyer-recommended attorneys. Never sign first and review later — and don’t let anyone convince you legal review is unnecessary.

Attorney fees on Long Island typically range from $1,500–$3,500 depending on transaction complexity. That cost is minimal compared to equity loss from predatory contracts. Your attorney is your primary defense against fraud.

Advisory Note: Attorney fees vary based on transaction complexity, property circumstances, and the specific firm. Request a fee estimate in writing before engaging counsel.

Additional Warning Signs to Watch

Beyond the five major red flags, these secondary signals also indicate problems:

Vague or Missing Company Information

- No physical address (only PO boxes)

- Can’t find business registration in state records

- Website created recently with minimal content

- No online reviews or verifiable track record

- Company name changes frequently

- No professional email domain (using Gmail/Yahoo)

Communication Red Flags

- Avoiding direct answers to specific questions

- Providing inconsistent information across conversations

- Refusing to communicate in writing

- Using high-pressure sales language

- Making unrealistic promises about timelines or prices

- Contacting you excessively after initial inquiry

Financial Red Flags

- Offers significantly below market value without clear explanation

- Requests to split proceeds in unusual ways

- Suggests “creative” financing arrangements

- Asks you to falsify documentation

- Proposes taking title before paying full proceeds

- Wants you to move out before closing

Process Red Flags

- Rushes through explanations without ensuring understanding

- Discourages property appraisals or evaluations

- Suggests hiding the transaction from family members

- Recommends against getting competing offers

- Uses unlicensed “consultants” instead of attorneys

- Proposes using their title company exclusively

Real Long Island Scam Examples

These scenarios from Nassau and Suffolk County demonstrate how red flags appear in practice.

The Foreclosure Rescue Scam

A Patchogue homeowner facing foreclosure received a “rescue” offer. The company promised to pay off his mortgage, let him stay in the home, and allow him to buy it back within two years.

Red flags present:

- Demanded signature within 48 hours (pressure tactic)

- Required $500 “processing fee” (upfront payment)

- Contract included complex rent-back terms (escape clauses)

- Discouraged attorney review (avoiding legal scrutiny)

Reality: After signing, he discovered he’d transferred his deed for $50,000 below market value, owed “rent” exceeding his previous mortgage, and the buyback option required impossible conditions. He lost his home and equity.

Protection: He should have consulted a foreclosure attorney immediately. New York is a judicial foreclosure state under NY RPAPL Article 13 — the process can take 2–5+ years, meaning homeowners often have more time than scammers imply. Free foreclosure prevention counseling is also available through the NYS Department of Financial Services.

The Wholesaler Bait-and-Switch

A Nassau County widow inherited her husband’s home and received a $380,000 cash offer. The contract included “buyer or assigns” language she didn’t understand.

Red flags present:

- No proof of funds provided despite requests (inability to close)

- Contract allowed assignment (wholesaler operation)

- Price reduced to $340,000 three days before closing (bait-and-switch)

- Claimed “inspection revealed issues” never mentioned initially (fabricated renegotiation)

Reality: The “buyer” was a wholesaler who found an actual investor at $365,000, keeping $25,000 by reducing her price. She had stopped marketing to other buyers, leaving her with little leverage.

Protection: Demanding proof of funds and attorney review of “assigns” language would have exposed the wholesaling scheme early.

The Fee Collection Scheme

A Huntington homeowner received multiple offers after advertising FSBO. One buyer seemed most professional but requested a $750 “appraisal and inspection fee,” a $300 “title search advancement,” and payment via wire transfer for “faster processing.”

Red flags present:

- Multiple upfront fees (classic fee scam)

- Wire transfer request (untraceable payment)

- No company verification provided (fraudulent operation)

- Pressure to pay quickly before “losing the slot” (artificial urgency)

Reality: After paying $1,050, the company disappeared. No offer ever materialized. She lost money and time.

Protection: Zero upfront fees is non-negotiable. Legitimate buyers never request seller payments before closing.

How to Protect Yourself: Action Steps

Before Engaging

Research the company thoroughly:

- Verify business registration with the NY Department of State

- Check Better Business Bureau ratings and complaints

- Search the company name with “reviews” and “complaints”

- Verify physical address via Google Street View

- Consider how long they’ve operated — a longer operating history generally indicates greater accountability and verifiable track record

Understand your property value:

- Research comparable sales in your neighborhood

- Get a property valuation from local realtors

- Understand that cash offers will typically be lower than retail market value

- Know the range you should expect given your property’s condition

Prepare questions to ask:

- Review essential questions for cash buyers before any conversation

- Write your questions down and note answers for comparison across buyers

During Initial Contact

Request proof of funds immediately:

- Don’t proceed without financial verification

- Call banks or lenders to verify documents using official contact numbers

- Ask for recent purchase closing statements

Watch for red flag language:

- Note any pressure tactics or urgency creation

- Question any upfront fee requests

- Identify escape clauses or contingencies

- Recognize attorney avoidance attempts

Get everything in writing:

- Verbal promises mean nothing

- Request written offers before committing

- Ensure offers include all terms discussed

Before Signing

Hire independent legal counsel:

- Find an attorney experienced in New York real estate

- Never use buyer-recommended attorneys

- Give your attorney adequate review time (3–5 days minimum)

Get multiple offers:

- Contact 3–5 different cash buyers

- Compare offers, terms, and timelines

- Use competing offers for leverage

Trust your instincts:

- If something feels wrong, it probably is

- Don’t let pressure override caution

- Walk away from any situation that creates discomfort

Understanding when selling to an investor makes sense helps you distinguish between legitimate services and exploitative schemes.

Questions to Ask That Expose Scammers

Financial Questions

“Can you provide proof of funds right now?” Legitimate answer: “Absolutely, I’ll email bank statements within the hour.” Scam answer: Delays, excuses, or refusal.

“What fees will I pay at closing?” Legitimate answer: “Only transfer taxes, title costs, and your attorney — I can walk you through typical closing costs.” Scam answer: Mentions assignment fees, processing fees, or other pre-closing charges.

Advisory Note: Closing costs vary by transaction. The figures quoted by any buyer should be confirmed in writing and reviewed by your independent attorney before you sign.

“How did you calculate this offer?” Legitimate answer: Detailed breakdown with repair costs and comparable sales. Scam answer: Vague “based on our analysis” without specifics.

Process Questions

“How long is this offer valid?” Legitimate answer: “5–7 days to give you time for due diligence.” Scam answer: “24–48 hours” or “need to know today.”

“Should I have an attorney review this?” Legitimate answer: “Absolutely, I insist you have independent legal counsel.” Scam answer: “Not really necessary for simple transactions.”

“Can I get competing offers before deciding?” Legitimate answer: “You should definitely get multiple offers for comparison.” Scam answer: “This is the best offer you’ll receive” or immediate pressure to commit.

Company Questions

“How long have you been buying properties?” Legitimate answer: Specific years with a verifiable track record. Scam answer: Vague responses or a very recent startup with no history.

“Can you provide references from past sellers?” Legitimate answer: Contact information for 3–5 recent clients. Scam answer: Privacy excuses or refusal.

“What’s your company’s physical address?” Legitimate answer: An actual office location you can verify. Scam answer: PO box only or a residential address.

Ready to Sell Safely?

Recognizing cash home buyer scams to avoid protects your property equity from predatory operators. The five critical red flags—pressure tactics, upfront fees, no proof of funds, contingent contracts, and attorney avoidance—signal danger requiring you to walk away.

Legitimate cash buyers exist and provide valuable services for Long Island homeowners facing foreclosure, divorce, estate settlement, or property condition challenges. Professional investors operate transparently, encourage legal representation, provide proof of funds immediately, use clean contracts without escape clauses, and give you time for informed decisions.

The Property Father embodies these legitimate practices. We provide written offers with detailed explanations, insist on attorney involvement, accommodate your timeline, and honor our commitments without surprise reductions or hidden fees.

Get a fair, no-obligation offer in 24 hours. We’ll answer every question, provide complete financial documentation, and give you time to make confident decisions.

See our Long Island Home Selling Guide for a complete breakdown of your options.