Last Updated: May 2026

Not every home sale follows the same path. While most homeowners automatically assume listing with a realtor is the “right” way to sell, specific situations exist where selling to an investor vs. listing with an agent delivers better financial outcomes, faster timelines, and less stress. Understanding when selling to an investor makes sense versus listing traditionally could save you months of hassle and thousands in unexpected costs.

In 2026, Long Island homeowners facing property challenges, time constraints, or financial pressure increasingly discover that the traditional listing route — requiring repairs, showings, and uncertain timelines — simply doesn’t fit their circumstances. Real estate investors offer an alternative that bypasses these obstacles entirely, purchasing properties as-is with agreed-upon closing dates. The key is recognizing which situations genuinely benefit from investor sales versus which homes should hit the open market.

Investor vs Traditional Listing

When Does Each Make Sense?

Choose Investor

Needs $25K+ repairs

Major system issues

Foundation/roof problems

Need close in 60 days

Facing foreclosure

Job relocation

No repair funds

Can’t carry 2 mortgages

Need guaranteed close

Choose Listing

Move-in ready

Updated throughout

No major repairs needed

Have 4-6 months

No time pressure

Can wait for right buyer

Afford carrying costs

Want max price

Can handle uncertainty

Real Cost Comparison

$450K home needing $40K repairs

7-9 months

$40K upfront needed

7-14 days

$0 upfront needed

Investor Sales Excel For:

• Divorce (avoid conflicts)

• Inherited property (multiple heirs)

• Major repairs (no capital)

• Probate sales (court timelines)

The Traditional Listing Path: When It Works Best

Before examining when investors make more sense, let’s establish when traditional listing is the optimal choice. Understanding this baseline helps you recognize when your situation diverges from the ideal listing scenario.

Perfect Listing Candidates

Traditional listings work exceptionally well when:

Your property is in excellent condition. Move-in ready homes with updated kitchens, modern bathrooms, new roofs, and functioning systems attract traditional buyers willing to pay premium prices. These properties photograph beautifully, show well, and generate multiple offers in competitive markets.

You have 3–6 months available. The traditional sale process involves preparation (1–2 weeks), active marketing (2–4 weeks), negotiation and inspection (2–4 weeks), buyer financing (4–6 weeks), and closing (2–4 weeks). If your timeline accommodates this 90–180 day journey — and timelines may extend in slower market conditions — listing makes sense.

You can afford carrying costs during the sale. Mortgage payments, property taxes, insurance, utilities, and maintenance continue throughout the listing period. Carrying cost estimates vary based on your remaining mortgage balance, Nassau or Suffolk County property taxes, and insurance premiums, but can add up significantly over several months. If you can comfortably cover these costs, traditional listing remains viable.

The local market favors sellers. In active Long Island real estate markets with low inventory and high demand, well-priced homes sell quickly at or above asking price. Strong seller’s markets maximize traditional listing success.

You want to test for absolute maximum price. If getting every possible dollar matters more than speed or certainty, listing allows you to gauge market interest and potentially receive offers above asking price in competitive situations.

For homeowners meeting these criteria, listing with an experienced Nassau County or Suffolk County agent makes perfect sense. But many situations fall outside these ideal parameters.

When Property Condition Demands a Different Approach

Property condition represents the single biggest factor determining whether investors or traditional listings make more sense.

Major Repairs That Kill Traditional Sales

Certain property issues create nearly insurmountable obstacles for traditional buyers who rely on financing. Lenders refuse to fund purchases when properties have:

Foundation problems. Cracks, settling, water intrusion, or structural concerns trigger lender red flags. Repair estimates ranging from $15,000–$40,000 (approximate ranges for Long Island as of 2025–2026; costs will vary by contractor, scope, and property) scare away traditional buyers, while FHA loans often won’t approve financing until foundation issues are resolved.

Roof damage. Roofs with less than 3–5 years of remaining life require replacement before most lenders approve financing. A $15,000–$25,000 roof replacement bill eliminates most buyer pools. Even if buyers agree to repairs, coordinating contractor work during the sale process creates delays and complications.

Outdated electrical systems. Homes with knob-and-tube wiring, 60-amp service, or ungrounded outlets fail modern safety inspections. Upgrading electrical systems costs $3,000–$15,000 and requires permits, inspections, and potential drywall repairs — all while the property sits unlisted.

Plumbing issues. Galvanized pipes, polybutylene plumbing, main line problems, or septic system failures require immediate attention before traditional sales can proceed. Costs range from $3,000–$20,000 depending on scope.

HVAC system failure. Non-functioning heating or cooling systems must be replaced ($8,000–$15,000) before most buyers or their lenders will approve the sale. During Long Island winters, homes without working heat fail inspections automatically.

Code violations. Unpermitted additions, illegal conversions, zoning violations, or open permits create title issues that prevent traditional closings. Resolving these problems takes months and thousands in legal and contractor fees.

When facing these issues, selling to an investor who purchases as-is eliminates the need to fund repairs upfront. Understanding what selling as-is means helps homeowners realize they don’t need perfect properties to sell successfully.

Cosmetic Condition That Impacts Marketability

Even without major structural issues, cosmetic condition dramatically affects traditional sale potential:

Dated interiors from the 1970s–1990s. Popcorn ceilings, laminate countertops, linoleum floors, and harvest gold appliances don’t prevent sales, but they significantly reduce buyer interest and sale prices. Updating these elements costs $20,000–$60,000 — money most sellers lack before listing.

Deferred maintenance throughout. Properties showing years of neglect — peeling paint, overgrown landscaping, worn carpets, stained fixtures — struggle to generate buyer interest. First impressions matter enormously in traditional sales, and cosmetically challenged homes languish on the market.

Unusual layouts or configurations. Choppy floor plans, awkward additions, or non-standard room configurations limit buyer appeal. While structurally sound, these properties challenge traditional buyers seeking turnkey homes.

For properties requiring more than $30,000 in improvements before listing successfully, selling to an investor often nets comparable proceeds without upfront capital investment or months of construction chaos.

Time-Sensitive Situations Where Speed Trumps Price

Certain life circumstances create urgency that traditional listing timelines cannot accommodate.

Foreclosure and Financial Distress

Facing foreclosure on Long Island creates a ticking clock that can eliminate traditional listing as a viable option. Because New York is a judicial foreclosure state — a process that can take 2–5+ years under NY RPAPL Article 13 — homeowners need to understand exactly where they stand in the process before assuming they are out of time. If you are approaching a court-ordered sale date, the 4–6 month traditional listing process may not work mathematically.

Advisory Note: Foreclosure timelines in New York vary significantly based on where your case stands in the judicial process. Consult a licensed New York real estate attorney to determine your actual stage before making any sale decision.

Investors who can close in 7–14 days allow homeowners to:

- Potentially avoid foreclosure completing on their credit report — foreclosure can reduce your credit score by 85–160 points depending on your starting score, with the most severe impact in the first 2–3 years of the 7-year reporting period

- Recover equity remaining in the property

- Negotiate directly with the lender for cooperation

- Move forward without the ongoing burden of a foreclosure proceeding

Even if a traditional sale theoretically nets more, the speed and certainty of investor sales can outweigh potential price differences in distressed circumstances.

Job Relocation and Transfer

Relocating for work often comes with tight timelines — 30 to 60 days to start a new position in a different state. Carrying two mortgages while managing a long-distance traditional sale creates financial and logistical challenges.

Investor sales solve this by:

- Closing before the move date

- Eliminating the need for return trips for showings, inspections, or closing

- Avoiding double mortgage payments

- Providing certainty when timing the purchase of a new home in the relocation city

When your employer expects you in California in 45 days, waiting 5–6 months for a traditional Long Island sale doesn’t work.

Divorce Property Settlement

Selling during divorce on Long Island introduces unique challenges that often make investor sales preferable:

Emotional factors. Ex-spouses rarely want to coordinate repairs, staging, showings, and negotiations together. The friction and ongoing contact required for traditional sales can exacerbate already strained relationships.

Court-ordered deadlines. Divorce decrees often specify timelines for property disposition. Under New York Domestic Relations Law, marital property generally requires both parties’ consent to sell unless a court order directs otherwise — missing court-specified deadlines can trigger contempt proceedings or force unfavorable settlements.

Need for clean breaks. Both parties want to move forward, not remain tethered to a jointly-owned property requiring ongoing communication and decisions. Investor sales that close in 7–14 days provide the clean break both parties often seek.

Equity division disputes. When ex-spouses disagree on property value, pricing strategy, or timing, a third-party investor offer provides an objective figure both parties can accept or reject without ongoing conflict.

Inherited Property and Estate Settlement

Selling an inherited house or navigating probate sales in Suffolk County creates complications traditional sales can’t always easily accommodate:

Multiple heirs with conflicting interests. When siblings or family members inherit property together, disagreements about repairs, pricing, timing, and proceeds distribution can derail traditional sales. One heir living across the country, another wanting to move quickly, and a third hoping to maximize proceeds creates gridlock.

Estate debts and liabilities. Outstanding mortgages, liens, property taxes, or creditor claims against the estate require resolution. Traditional sales that take 4–6 months allow costs to accumulate while heirs remain liable.

Properties in disrepair. Inherited homes often reflect years of aging or deferred maintenance. Out-of-state heirs may lack the time, proximity, or funds to coordinate extensive repairs before listing.

Probate court timelines. Prolonged traditional sales can increase legal costs and complicate estate settlement under NY Surrogate’s Court proceedings. Quick investor sales can satisfy estate parties’ need for timely closure, though the executor’s ability to sell will depend on whether Letters Testamentary or Letters of Administration have been issued.

Advisory Note: New York probate timelines and the executor’s authority to sell vary by estate complexity and court schedule. Consult a New York estate attorney before committing to any sale timeline.

Financial Considerations: When the Math Favors Investors

Sometimes the numbers themselves reveal that investor sales deliver superior outcomes despite lower gross sale prices.

The True Cost Comparison

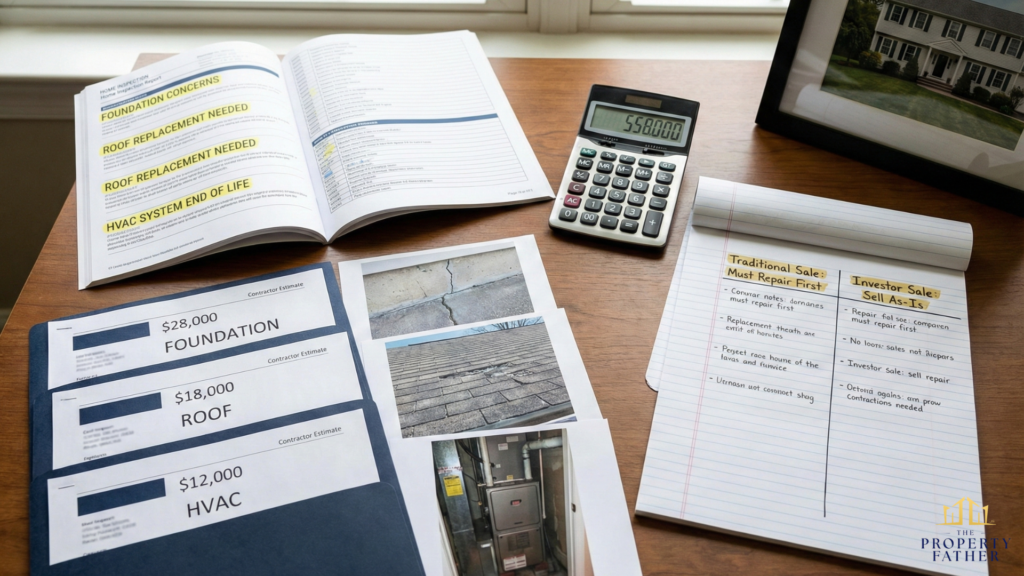

Consider a $450,000 Long Island home needing $40,000 in repairs:

Traditional Listing Path:

- Expected list price (after repairs): $490,000

- Commission (5.5%): -$26,950

- Repair costs: -$40,000

- Carrying costs during repairs and sale (6 months): -$18,000

- Staging, photography, marketing: -$2,500

- Net proceeds: $402,550

- Timeline: 7-9 months

- Risk: Buyer financing may fall through

Investor Sale Path:

- Cash offer (as-is): $395,000

- Commission: $0

- Repair costs: $0

- Carrying costs (2 weeks): -$1,200

- No staging or marketing: $0

- Net proceeds: $393,800

- Timeline: 7-14 days

- Risk: Zero (guaranteed close)

The traditional listing nets only $8,750 more while requiring $40,000 upfront, 7-9 months, and uncertain outcomes. For homeowners without $40,000 in cash reserves or the ability to wait 9 months, the investor sale is mathematically superior.

Hidden Costs That Erode Traditional Sale Value

Beyond obvious commissions and repairs, traditional sales accumulate costs that aren’t always budgeted upfront:

Carrying costs multiply over time. Each additional month of ownership means ongoing mortgage, tax, insurance, and utility payments. A sale that extends from 4 months to 7 months can cost significantly more than anticipated.

Buyer-requested repairs post-inspection. Even well-maintained homes generate inspection repair requests. Negotiations often result in price reductions or seller-funded repairs that weren’t anticipated.

Deal fallthrough costs. When buyers walk away after inspection or financing fails, you’ve lost 60–90 days plus incurred inspection fees, appraisal costs, and attorney fees — all while continuing to pay carrying costs.

Price reductions over time. Homes sitting on market beyond 45–60 days often require price reductions to maintain buyer interest. These reductions can offset or exceed any theoretical premium over investor offers.

Understanding the true cost of selling with a realtor reveals that net proceeds matter far more than gross sale prices.

Avoiding Common Pitfalls When Considering Investors

Not all investor transactions are created equal. Understanding how to evaluate offers protects homeowners from predatory practices.

Red Flags to Avoid

Wholesalers pretending to be buyers. Some “investors” are actually wholesalers who don’t purchase properties directly — they assign contracts to actual buyers for a fee. This adds uncertainty and potential renegotiation. True investors have funds ready and close directly.

Unrealistic timeline promises. Even cash sales in New York require title searches, attorney review, and documentation. Legitimate investors typically close in 7–14 days — fast, but not instantaneous. Be cautious of anyone claiming same-day or next-day closings.

Pressure tactics. Reputable investors provide written offers with no obligation and give you time to consult attorneys or financial advisors. High-pressure tactics or demands for immediate commitment are among the cash home buyer scams to avoid.

Lowball offers without justification. Professional investors explain how they calculated their offer, including repair costs, market comparables, and their margin. Offers without transparent reasoning may be artificially low.

Questions to Ask Before Accepting

Protect yourself by asking these questions:

- How do we buy houses companies work? Request a clear explanation of their process.

- Are we buy houses companies legit? Ask for proof of funds, business licenses, and references from past sellers.

- Do cash buyers pay fair prices? Request the comparable sales they used to determine their offer.

- What questions should I ask cash buyers? Prepare a list covering timeline, contingencies, and closing costs.

- Can I choose my closing date? Flexibility with timing indicates a legitimate buyer focused on your needs.

Knowing why cash offers are lower than retail prices helps you evaluate whether offers are fair given your circumstances.

Real Long Island Examples: When Investors Made Sense

Examining actual scenarios illuminates when investor sales provide superior outcomes.

Case Study 1: Suffolk County Foundation Issues

A Patchogue homeowner discovered foundation cracks during a pre-listing inspection. Structural engineer estimates came back at $28,000 for repairs. The home, valued at approximately $425,000 in good condition, would not qualify for most buyer financing until repairs were completed.

Traditional listing option: Invest $28,000 in foundation repairs, list at $425,000, pay estimated commission costs, wait 4–6 months. Illustrated net after commissions and repairs: approximately $373,625 — before accounting for carrying costs, inspection negotiations, or potential buyer-financing contingencies.

Investor option: Accept as-is cash offer of $360,000, close in 10 days with no repairs or staging. Net after minimal closing costs: approximately $358,000.

Decision: She chose the investor sale, avoiding $28,000 in upfront capital she didn’t have, eliminating months of carrying costs, and gaining certainty of close. When total avoided costs are factored in, the “lower” offer compared favorably on a net basis.

Study 2: Nassau County Divorce Sale

A Nassau County couple going through divorce owned a $520,000 home needing $15,000 in cosmetic updates. They disagreed on whether to make improvements, how to price the property, and who would manage the sale process.

Listing complications: Coordinating repairs while separated, managing showings at the marital home, negotiating jointly with buyers, waiting 4–6 months while both remained financially entangled.

Solution: Accepted a $475,000 cash offer with a 14-day close. Each received their equity share quickly, allowing both to move forward separately. The simplified process eliminated ongoing conflict and provided clean closure.

Study 3: Inherited Huntington Property

Three siblings inherited a Huntington home from their parents. One lived locally, one in California, and one in Florida. The 1960s ranch needed updating throughout — kitchen, bathrooms, flooring, paint. Estimated improvement costs: $45,000.

Listing challenges: Coordinating repairs from three states, funding improvements from estate accounts, managing contractor work remotely, waiting 5–7 months while paying carrying costs and estate attorney fees.

Outcome: Sold as-is for $380,000 with an 8-day close. Each sibling received their one-third share promptly. The avoided out-of-state travel, coordination overhead, and prolonged estate settlement made the investor sale clearly preferable for this family’s circumstances despite a lower gross price.

Making Your Decision: A Framework

Use this framework to determine whether your situation favors investor sales:

Investor Sales Make More Sense When:

Property condition:

- Repairs exceed $25,000

- Structural, foundation, or major system issues exist

- Permits, code compliance work, or title curing required

- Cosmetically dated but functionally sound

Timeline needs:

- Closing needed in under 60 days

- Facing foreclosure, job relocation, or court deadlines

- Cannot afford extended carrying costs

- Certainty valued over maximum price

Financial situation:

- You lack funds for pre-listing repairs

- Cannot carry two mortgages

- Need proceeds quickly for another purchase or obligation

- Value guaranteed closing over potential higher offers

Personal circumstances:

- You’re settling an estate with multiple heirs

- Managing divorce-related property division

- Overwhelmed by the prospect of traditional sale management

- Live out of state or far from the property

Listings Make More Sense When:

- Your home is in excellent, move-in ready condition

- Have 4-6+ months available for the sale process

- Can afford all carrying costs during marketing

- Have capital for any needed cosmetic improvements

- Want to test the market for absolute maximum price

- The local market strongly favors sellers

- You’re comfortable managing showings, negotiations, and contingencies

Ready to Sell Your Long Island Home?

When does selling to investor make sense? The answer depends on your property condition, timeline, financial situation, and personal circumstances. For many Long Island homeowners facing repairs, time pressure, or complex situations like foreclosure, probate, or inherited property, selling to an investor delivers better net outcomes with far less stress.

If your situation aligns with the investor-favorable scenarios outlined above, a cash offer might be your best path forward. Get a fair, no-obligation offer in 24 hours and close in as little as 7 days—no repairs, showings, or risk.

See our Long Island Home Selling Guide for a complete breakdown of your options.