You’ve seen the signs on telephone poles, banners along highways, and ads on social media: “We Buy Houses – Cash – Any Condition – Fast Close.” For homeowners facing foreclosure, inheriting unwanted property, or needing to sell quickly, these offers seem like lifelines. But skepticism is healthy—are we buy houses companies legit, or are they predatory scammers targeting desperate sellers?

The answer isn’t simple. The cash home buying industry includes both legitimate investors providing valuable services and unethical operators exploiting homeowner distress. In 2026, Nassau and Suffolk County homeowners need clear criteria to distinguish between professional companies offering fair deals and bad actors employing deceptive tactics. This guide provides the specific verification steps, red flag warnings, and questions to ask that protect you while helping you identify trustworthy buyers who can genuinely solve your property challenges.

Legit vs Scam Cash Buyers

How to Tell the Difference

✓ Legitimate Buyers

• Explain pricing transparently

• No upfront fees ever

• Encourage attorney review

• Honor written offers

• No pressure tactics

• 3+ years track record

• Verifiable references

✗ Scam Operators

• Vague about pricing method

• High-pressure urgency

• Discourage legal advice

• Last-minute price drops

• “Sign now or lose deal”

• No verifiable history

• Won’t show proof of funds

5-Step Verification

Verify with NY Dept of State

Bank statements or lender letters

BBB rating, Google reviews, website

Contact 3-5 past sellers

Have lawyer review all contracts

🚨 Walk Away If They:

• Request any upfront payment

• Won’t provide proof of funds

• Discourage attorney consultation

• Use contingent contracts

• Can’t explain their offer

Understanding the “We Buy Houses” Business Model

Before evaluating individual companies, understanding how legitimate cash buying works helps you recognize proper operations.

How Legitimate Cash Buyers Operate

Professional real estate investors purchase properties directly from homeowners, renovate them, and resell at retail prices. Their business model depends on:

Accurate property valuation. They evaluate your home’s current condition, calculate repair costs, estimate after-repair value based on comparable sales, and determine their purchase price by subtracting these costs plus a profit margin.

Fast, certain closings. Unlike traditional buyers needing financing approval, investors use cash or pre-arranged funding that eliminates appraisal contingencies, loan denial risks, and extended timelines.

As-is purchases. They buy properties in any condition without requiring sellers to make repairs, clean, or stage. This serves homeowners who lack capital for improvements or time for traditional sales.

Win-win transactions. Legitimate investors solve genuine problems — helping homeowners in foreclosure, divorce, or probate situations exit quickly while making reasonable profits through renovation and resale.

Both the FTC and the CFPB publish consumer guidance on how to identify legitimate cash buyers and spot warning signs — reviewing these resources is worthwhile before engaging with any buyer.

Why Offers Are Lower Than Retail

Understanding why cash offers are lower than list price is essential context for evaluating any offer.

Advisory Note: The following is an illustrative example of how a cash buyer may calculate an offer. It is not a standard formula or a benchmark for evaluating any real offer you receive. Actual deductions vary widely based on repair scope, local market conditions, and individual buyer margins.

A home worth $450,000 in perfect condition might receive a $360,000 cash offer because:

- Repair costs: $40,000

- Holding costs during renovation: $8,000

- Transaction costs (buying + selling): $15,000

- Profit margin (varies by buyer and market): approximately $27,000 in this example

Total deductions from retail value: $90,000

This isn’t necessarily a “lowball” — it reflects business math. Legitimate investors explain their calculations transparently. Dishonest operators don’t.

Red Flags: Signs of Illegitimate Operators

Certain behaviors immediately identify companies you should avoid.

High-Pressure Tactics

Demanding immediate signatures. Legitimate buyers provide written offers with no obligation and give you time to consult attorneys or family members. Operators saying “this offer expires in one hour” or “sign now or we withdraw” are creating false urgency to prevent you from seeking legal advice or comparing offers.

Refusing to provide proof of funds. Professional investors immediately provide bank statements or pre-approval letters showing they can close. Anyone refusing this basic verification cannot reliably deliver on their promises.

Aggressive marketing that exploits fear. While advertising is normal, targeting homeowners in distress with manipulative messaging like “You’re out of time!” or “Sign or lose everything!” crosses ethical lines. Legitimate companies educate and inform; predators intimidate.

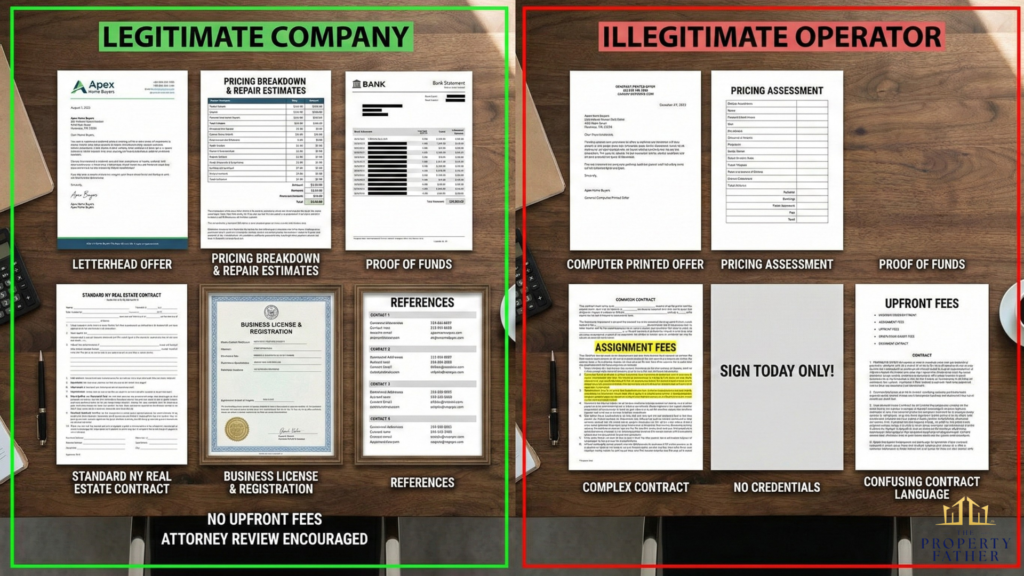

Deceptive Contract Terms

Hidden fees or junk fees. Watch for contracts including “assignment fees,” “processing fees,” “due diligence fees,” or other charges reducing your net proceeds. Legitimate buyers absorb these costs.

Last-minute price reductions. Ethical investors honor their written offers. Bad actors make attractive initial offers, then discover “unexpected issues” just before closing, pressuring desperate sellers to accept reduced prices.

Complex contracts obscuring terms. Professional investors use standard New York real estate contracts that attorneys can easily review. Convoluted custom contracts with confusing language can hide unfavorable terms.

Wholesaler Misrepresentation

One of the most common issues in the “we buy houses” industry involves wholesalers misrepresenting themselves as actual buyers. Understanding the cash buyer vs. wholesaler difference protects you before you sign anything.

What wholesalers actually do: They contract your property at one price, then immediately market it to actual investors at a higher price, pocketing the difference. They never intend to purchase your home — they are middlemen assigning contracts, not buyers.

Why this matters: Wholesalers often lack funds to close if they can’t find an end buyer, may renegotiate prices downward when their investors demand it, create unnecessary delays, and provide no certainty of closing.

How to identify them: Contracts containing “and/or assigns” or language like “subject to partner approval” are strong indicators of wholesaling intent. Ask directly: “Will your company be purchasing this property, or do you intend to assign the contract to another buyer?” Legitimate buyers purchase directly and put their company name on the contract.

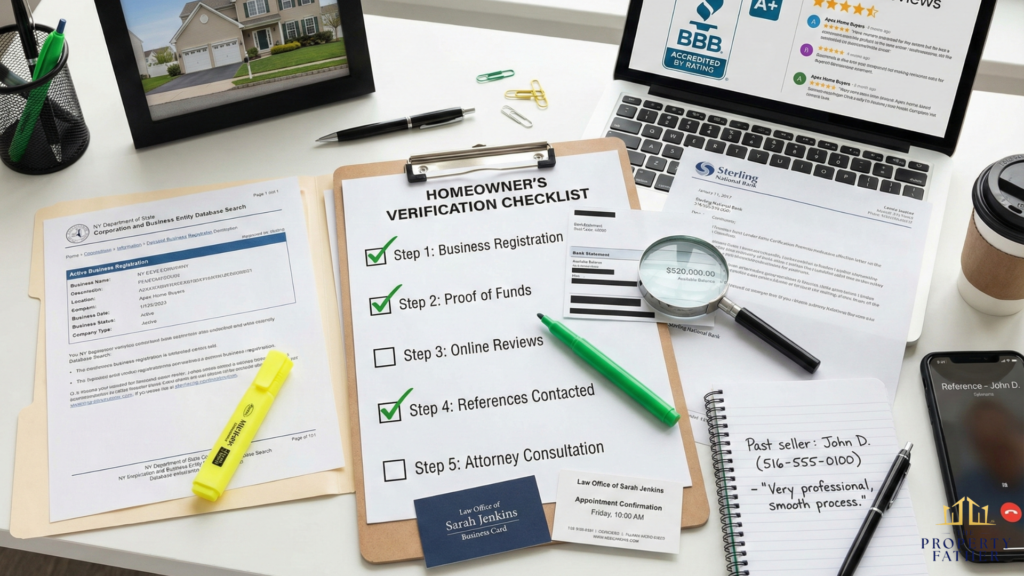

Verification Steps: How to Vet Any Cash Buyer

Take these specific steps before accepting any offer. A full checklist of questions to ask a cash buyer provides additional guidance.

Check Business Credentials

Verify business registration.

- Search the New York State business entity database for the company

- Confirm they’re registered, active, and in good standing

- Check how long they’ve been in business (3+ years indicates stability)

Review online presence.

- Professional website with actual office address and phone

- Google Business listing with reviews and responses to feedback

- Social media presence showing ongoing operations

- Better Business Bureau rating and complaint history

Confirm real estate licenses (if applicable).

- In New York, anyone acting as a broker “for another and for a fee” must be licensed

- Verify any claimed license through the NY DOS Division of Licensing Services

- Note: Investors purchasing property directly for their own account are not required to hold a real estate broker license under NY Real Property Law §440-a

Request and Verify Financial Proof

Demand proof of funds. Every legitimate buyer provides:

- Bank statements showing available cash

- Pre-approval letters from lenders

- Previous closing statements from recent purchases

Verify with their bank or lender. Don’t just accept documents at face value — call the institution directly using phone numbers from their official websites, not numbers printed on provided documents.

Check recent purchase history. Ask for addresses of recent acquisitions. In Nassau and Suffolk County, closed property sales are recorded with the County Clerk and can be verified through public records searches to confirm a buyer actually closed on properties they claim to have purchased.

Interview and Question

Ask these specific questions to ask a cash buyer and evaluate their responses:

“How do you calculate your offers?” Legitimate answer: Detailed explanation using comparable sales, repair estimates, and their margin. Red flag: Vague responses or refusal to explain methodology.

“Can you provide references from past sellers?” Legitimate answer: Contact information for 3–5 recent sellers willing to share their experiences. Red flag: Refusal or excuses about privacy without offering alternatives.

“What’s your timeline from offer to closing?” Legitimate answer: A specific timeline — typically 10–14 days for New York cash transactions — with a clear explanation of steps including title search, attorney review, and closing coordination. Red flag: Unrealistic promises of 24–48 hour closes, or vague timelines.

“Are there any fees I’ll pay at closing?” Legitimate answer: Only standard closing costs (attorney, transfer taxes) — disclosed upfront. Red flag: Assignment fees, inspection fees, or surprise charges.

“Is this offer contingent on anything?” Legitimate answer: No contingencies beyond a standard title search. Red flag: Contingent on partner approval, financing, or ability to assign the contract.

“Will your company be purchasing this property directly?” Legitimate answer: “Yes — we are the buyer and will purchase directly.” Red flag: Hesitation, or an explanation involving assigning the contract to another investor.

Learning what questions to ask cash buyers protects you from bad actors.

Legitimate Company Characteristics

Professional cash buyers share these common traits.

Transparency in All Dealings

Clear, written offers. They provide detailed written offers explaining how they calculated the price, what repairs they factored in, the expected closing timeline, and any conditions.

No pressure, no manipulation. They encourage you to consult with attorneys before signing, get multiple offers from other buyers, take time to make informed decisions, and ask questions at any point.

Open communication. They respond to inquiries promptly, provide direct contact information for decision-makers, and maintain consistent communication throughout the process.

Professional Operations

Established business infrastructure:

- Physical office location (not just a PO box)

- Professional staff including transaction coordinators

- Relationships with reputable attorneys and title companies

Track record of completed transactions:

- Can provide documentation of recent closings

- Public records confirm a history of purchases

- Positive reviews from past clients with verifiable details

Ethical marketing practices:

- Truthful advertising without deception

- Clear identification of their business model

- Respect for homeowners’ circumstances

- No harassment or excessive contact

Fair Pricing and Terms

While cash offers are lower than retail, legitimate buyers explain their pricing methodology transparently, base offers on objective market data and repair estimates, honor their written offers without last-minute reductions, and accommodate reasonable seller requests around timing.

Understanding whether cash buyers pay fair prices requires evaluating offers against your specific circumstances and market conditions.

Common Scams and How to Avoid Them

Be aware of these specific fraudulent schemes targeting Long Island homeowners.

The Foreclosure Rescue Scam

How it works: Scammers target homeowners facing foreclosure, promising to “save” their home. They have homeowners sign documents transferring the deed while promising they can stay in the home and eventually buy it back. The homeowner loses ownership, the scammer collects any equity, and the homeowner faces eviction.

How to avoid: Never sign over your deed while remaining in the property. The CFPB specifically identifies schemes that ask you to transfer title to your home while promising a rent-back and buy-back arrangement as a recognized foreclosure rescue scam. The FTC’s mortgage relief scam guidance reinforces this: if you transfer the deed, you are not likely to get it back.

The Fee Scam

How it works: A company requests upfront fees for “property evaluation,” “inspection,” “processing,” or “paperwork.” After collecting fees, they disappear or submit a lowball offer designed to be rejected.

How to avoid: Legitimate cash buyers never request upfront fees. They make money from purchasing and reselling properties, not from charging sellers fees at any stage of the process.

The Bait-and-Switch

How it works: An initial offer is attractive and gets you excited. Days before closing, they “discover” issues requiring a significant price reduction. Sellers who have already made moving plans often feel pressured to accept.

How to avoid: Get offers in writing. Work with buyers who conduct their property evaluation before submitting an offer — not days before closing. Understanding how cash home sales work helps you recognize normal timelines versus manufactured urgency.

The Equity Stripping Scheme

How it works: A buyer offers a price covering your mortgage but far below actual value. They pressure you to close quickly before you can research comparable sales or consult an advisor.

How to avoid: Always get your property evaluated by multiple buyers. Never accept a first offer without comparison shopping. Research comparable sales in your Nassau County or Suffolk County neighborhood before any signing.

How The Property Father Operates Legitimately

Understanding how professional cash buyers conduct business helps you evaluate any company.

Our Transparent Process

Step 1: Initial Contact

- You reach out via phone, website, or referral

- We gather basic property information

- No pressure, no commitment required

Step 2: Property Evaluation

- We schedule a convenient property visit

- Evaluate condition, needed repairs, and market value

- Research comparable sales in your specific Long Island neighborhood

Then, Step 3: Written Offer

- Provide a detailed written offer within 24–48 hours

- Explain our calculation methodology

- Include repair estimates and comparable sales used

- Specify closing timeline and any contingencies (typically none)

Step 4: Your Decision Period

- No pressure to accept immediately

- Encourage consultation with attorneys, family, and other buyers

- Answer any questions about terms or process

- Provide proof of funds upon request

Step 5: Contract and Closing

- Use standard New York real estate contracts

- Your attorney reviews all documents

- We coordinate with the title company and attorneys

- Close on your schedule — typically 10–14 days

- Wire funds same day as closing

What Sets Legitimate Buyers Apart

No hidden fees or surprises. The offer you receive is what you’ll get, minus only standard closing costs disclosed upfront.

Attorney involvement. We encourage you to have attorney representation to protect your interests.

Flexible closing timelines. Need more time? Moving early? We accommodate your schedule rather than forcing artificial urgency.

Educational approach. We explain your options, including situations where traditional listing might serve you better.

Understanding whether selling for cash is worth it depends on your circumstances — and requirements for selling your home to a cash buyer are less complex than many sellers expect.

When Cash Buyers Make Sense vs. When to Avoid

Not every situation requires cash buyer services, and legitimate companies acknowledge this.

Appropriate Situations for Cash Buyers

Time pressure exists:

- Foreclosure looming with court dates approaching

- Divorce settlement requiring quick resolution

- Job relocation with a tight timeline

- Estate settlement with court deadlines

Property condition challenges traditional sales:

- Major repairs needed (foundation, roof, systems)

- Outdated or unfinished spaces

- Code violations or permit issues

- Properties requiring extensive cleanup

Certainty matters more than maximum price:

- Can’t afford deal fallthrough risk

- Need guaranteed closing for a next purchase

- Want to avoid showing disruptions

- Value peace of mind over potential extra proceeds

Financial constraints exist:

- No capital for pre-listing repairs

- Can’t carry the property through an extended sale

- Facing financial hardship requiring quick equity access

When Traditional Listing Makes More Sense

Legitimate cash buyers will tell you when listing traditionally serves you better:

- Home is in excellent, move-in ready condition

- You have 4–6 months available for marketing and sale

- The local market strongly favors sellers

- You can afford carrying costs during the sale period

- Maximum sale price matters more than timeline or certainty

Questions You Should Ask (And Answers to Expect)

About Their Business

Q: “How long have you been buying houses?” Good answer: Specific years in business with a verifiable track record. Bad answer: Vague responses or a very recent start with no documented history.

Q: “How many Long Island properties have you purchased in the past year?” Good answer: A specific number with addresses you can verify via public records. Bad answer: Unwillingness to provide specifics or evidence.

Q: “Can you provide proof that you have funds to close?” Good answer: Immediate provision of bank statements or lender letters. Bad answer: Delays, excuses, or refusal to provide documentation.

About Their Offer

Q: “How did you calculate this offer?” Good answer: Detailed breakdown showing repair estimates, comparable sales, and margins. Bad answer: “It’s based on our analysis” without specifics.

Q: “Is this your final offer, or might it change?” Good answer: “This is our firm offer based on current property condition.” Bad answer: “We’ll need to inspect further before finalizing.”

Q: “What happens if you find issues during the title search?” Good answer: “We’ll work with you to resolve standard title issues.” Bad answer: “We’ll renegotiate the price.”

About the Process

Q: “What does your typical timeline look like?” Good answer: A specific timeline of approximately 10–14 days with steps clearly outlined — title search, attorney review, and closing. Bad answer: Unrealistic promises of 24-hour closings, or vague “as fast as you need.”

Q: “Do you encourage sellers to have attorney representation?” Good answer: “Yes — it’s standard practice in New York and we expect your attorney to review all documents.” Bad answer: “You don’t really need an attorney for this.”

Q: “Are there any fees I’ll pay?” Good answer: “Only standard closing costs: transfer taxes and your attorney fees.” Bad answer: Any mention of inspection fees, processing fees, or assignment fees.

Resources for Verification and Protection

Government Resources

New York Department of State: dos.ny.gov

- Verify business registration and status

- Look up real estate licenses

- Report fraudulent activity

Consumer Financial Protection Bureau: consumerfinance.gov

- Understand your rights as a homeowner

- Learn about common foreclosure rescue scams

- File complaints about predatory practices

Federal Trade Commission: consumer.ftc.gov

- Report fraud and deceptive practices

- Access consumer protection resources on mortgage and foreclosure scams

Professional Organizations

Better Business Bureau: Research company ratings and complaint history at BBB.org. Patterns of unresolved complaints are meaningful warning signs.

Local real estate attorney: Consult with an experienced New York real estate attorney before signing any contracts. In New York, having attorney representation in real estate transactions is standard practice and strongly advisable.

Online Research

- Search the company name plus “reviews” and “complaints”

- Review Long Island real estate market trends to understand fair pricing in context

- Research comparable sales in your neighborhood before accepting any offer

- Verify company addresses via Google Street View or Maps

- Check Nassau and Suffolk County Clerk public records for evidence of prior closings

Making Your Decision Confidently

Green Lights (Proceed with Confidence)

- Company has 3+ years of operating history

- Provides immediate proof of funds

- Uses transparent pricing methodology

- Encourages attorney consultation

- Has verifiable positive reviews

- Operates from a legitimate business address

- Answers all questions thoroughly and specifically

- No pressure tactics or urgency manipulation

Yellow Lights (Proceed with Caution)

- Newer company with limited track record (verify more carefully)

- Few online reviews (normal for smaller operations, but verify via public records)

- Offer seems lower than expected (get multiple offers to compare)

- Uses contract language worth attorney review

Red Lights (Walk Away Immediately)

- Requests any upfront fees

- Pressures for immediate signature

- Won’t provide proof of funds

- Uses “and/or assigns” language or “subject to partner approval” without disclosing wholesaling intent

- Can’t provide verifiable references

- Employs high-pressure or fear-based tactics

- Makes unrealistic timeline promises (such as same-day or next-day closings)

- Asks you to sign over your deed while remaining in the property

Ready to Sell Your Long Island Home?

Are we buy houses companies legit? The answer is yes—when they operate transparently, provide fair offers based on market realities, and prioritize your interests alongside their business needs. The key is knowing how to distinguish professional investors from predatory operators through verification steps, red flag awareness, and informed questioning.

If you’re facing a situation where traditional listing doesn’t work—tight timelines, property condition challenges, or need for certainty—working with legitimate cash buyers provides valuable solutions. The Property Father operates with full transparency, attorney involvement, and fair pricing based on actual market data.

Get a fair, no-obligation offer in 24 hours. We’ll explain our methodology, provide proof of funds, and give you time to make informed decisions. No pressure, no hidden fees, no surprises.

See our Long Island Home Selling Guide for a complete breakdown of your options.